Fifo and lifo inventory ppt powerpoint presentation gallery example

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Be able to fulfill all commitments with the help of our FIFO And LIFO Inventory Ppt Powerpoint Presentation Gallery Example. You will abide by your declarations.

People who downloaded this PowerPoint presentation also viewed the following :

Fifo and lifo inventory ppt powerpoint presentation gallery example with all 5 slides:

Focus on different careers with our FIFO And LIFO Inventory Ppt Powerpoint Presentation Gallery Example. Give them a good idea of all the exciting choices available.

FAQs for Fifo and lifo inventory ppt powerpoint

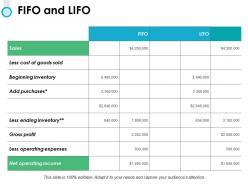

FIFO (First-In, First-Out) assumes oldest inventory is sold first, while LIFO (Last-In, First-Out) assumes newest inventory is sold first, creating different financial impacts during price fluctuations. These methods affect cost of goods sold, ending inventory values, and tax obligations differently, with many manufacturing and retail organizations finding that FIFO provides more accurate current asset valuations, while LIFO offers potential tax advantages during inflationary periods.

During inflation, FIFO increases net income by matching older, lower-cost inventory against current revenues, resulting in lower cost of goods sold. This accounting method enhances reported profitability while creating higher tax obligations, with many manufacturing and retail companies finding that FIFO delivers improved financial ratios and stakeholder confidence, ultimately strengthening competitive positioning in growth-focused markets.

LIFO is commonly used in industries experiencing rising costs, including oil and gas, steel manufacturing, automotive parts, and commodity trading sectors. These industries benefit from LIFO's ability to match current higher costs against revenues, reducing taxable income during inflationary periods, while providing better cash flow management and more accurate profit margins in volatile pricing environments.

FIFO typically shows higher profits and tax liabilities during inflation by matching older, cheaper costs against current revenues, while LIFO reduces taxable income by matching recent, higher costs against sales. These accounting methods significantly impact balance sheets, income statements, and cash flow, with many manufacturing and retail companies finding that LIFO delivers substantial tax savings during inflationary periods, ultimately enhancing operational efficiency.

FIFO inventory management offers significant advantages including accurate cost tracking, reduced obsolescence risk, enhanced cash flow predictability, improved financial reporting transparency, and better alignment with natural inventory flow patterns. This method enables businesses to minimize waste through systematic stock rotation, maintain fresher inventory levels, and deliver more reliable profit margins, with many retail and manufacturing organizations finding that FIFO streamlines operations while reducing carrying costs.

FIFO typically improves cash flow during inflationary periods by reporting lower cost of goods sold and higher profits, though this increases tax obligations. LIFO enhances cash flow by reducing taxable income through higher expenses, with many manufacturing and retail businesses finding that strategic inventory method selection significantly impacts their working capital management and operational efficiency.

During deflation, FIFO results in lower inventory valuations and higher cost of goods sold, while LIFO produces higher inventory values and lower COGS on financial statements. This occurs because FIFO assigns older, higher-priced items to sales first, while LIFO uses newer, lower-priced inventory, with many manufacturing and retail companies finding that FIFO provides more conservative earnings during deflationary periods.

Companies choose inventory accounting methods by evaluating their industry dynamics, tax implications, cash flow needs, and operational characteristics. Manufacturing firms often prefer FIFO for accurate current costs, while commodity businesses may select LIFO for tax advantages during inflation, with many organizations finding that their product lifecycle, storage requirements, and financial reporting goals ultimately determine the most strategic approach.

Switching from LIFO to FIFO typically increases inventory values, total assets, and retained earnings on the balance sheet, while potentially creating deferred tax liabilities during inflationary periods. This transition enhances financial ratios like current ratio and return on assets, with many companies finding that FIFO presents a stronger financial position to investors and creditors, ultimately improving access to capital.

FIFO typically results in higher inventory turnover ratios during inflationary periods by reflecting lower, older costs in inventory valuations, while LIFO shows lower turnover ratios with higher, recent costs remaining on balance sheets. These accounting methods significantly impact financial analysis and decision-making, with manufacturing, retail, and distribution companies finding that FIFO enhances apparent operational efficiency metrics and investor perceptions.

FIFO and LIFO serve as foundational costing methodologies within inventory management systems, automating valuation calculations, streamlining financial reporting, and ensuring regulatory compliance across different accounting standards. These automated systems enable businesses, particularly in manufacturing, retail, and pharmaceutical sectors, to maintain accurate cost tracking, optimize tax strategies, and deliver real-time inventory insights, ultimately enhancing operational efficiency and financial transparency.

FIFO and LIFO methods significantly influence pricing strategies by affecting cost calculations, profit margins, and competitive positioning in fluctuating markets. FIFO typically shows higher profits during inflation, enabling aggressive pricing strategies, while LIFO reflects current costs more accurately, helping companies maintain realistic pricing that covers replacement expenses and ultimately delivers sustainable profitability.

Companies must consider that LIFO is prohibited under International Financial Reporting Standards (IFRS), limiting global operations, while FIFO is universally accepted across all accounting frameworks. Additionally, tax regulations vary significantly by jurisdiction, with some countries restricting LIFO usage for tax purposes, and companies should evaluate compliance requirements, audit implications, and potential regulatory changes that could impact their chosen inventory valuation method's long-term viability.

International Financial Reporting Standards (IFRS) permit FIFO inventory valuation but explicitly prohibit LIFO, while U.S. GAAP allows both methods, creating significant reporting differences for multinational organizations. This divergence affects financial comparability, with companies operating across jurisdictions finding that FIFO adoption under IFRS often delivers more transparent inventory valuation and streamlined global reporting consistency.

FIFO and LIFO implementation best practices include accurate record-keeping systems, consistent application methods, regular audits, automated tracking technology, and clear staff training protocols. These approaches streamline inventory control by minimizing spoilage, ensuring tax compliance, and maintaining accurate cost calculations, with many retail and manufacturing organizations finding that strategic method selection ultimately delivers improved cash flow management and operational efficiency.

No Reviews