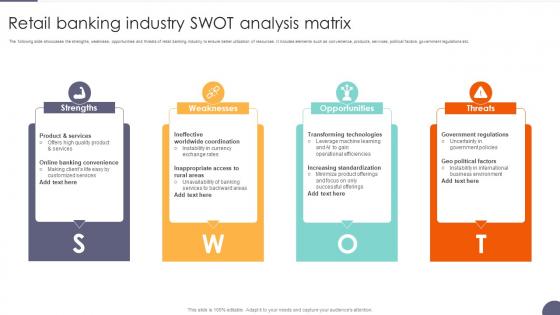

Retail Banking Industry SWOT Analysis Matrix

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

The following slide showcases the strengths, weakness, opportunities and threats of retail banking industry to ensure better utilization of resources. It includes elements such as convenience, products, services, political factors, government regulations etc.

People who downloaded this PowerPoint presentation also viewed the following :

Retail Banking Industry SWOT Analysis Matrix with all 6 slides:

Use our Retail Banking Industry SWOT Analysis Matrix to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Retail Banking Industry

Honestly, banks have some pretty solid advantages going for them. That customer base they've built up over decades? Pure gold. Plus all the regulatory stuff they've already figured out - new fintech companies are basically starting from scratch there. Branch networks still matter more than people think, especially for older folks who want face-to-face service. Most banks have decent apps now too. The revenue diversification helps when the economy gets weird. And let's be real - once you've got your mortgage, checking, savings all in one place, switching banks is such a pain that most people just... don't.

Banks are basically throwing everything they've got at making apps better these days. Photo check deposits are pretty standard now, plus those AI chat things answer your basic questions anytime. They're getting weirdly good at analyzing your spending to suggest stuff - honestly kind of invasive but also helpful? Voice commands and fingerprint logins are everywhere too. Biometric security feels very sci-fi but works great. The tricky part is they still need real humans for the big financial decisions. Nobody wants to get a mortgage from a robot, you know?

Honestly, customer service is what makes or breaks banks now. All the rates and products are basically the same everywhere, so how they treat you becomes everything. Trust matters huge when someone's handling your money, right? Happy customers stick around longer and actually buy more stuff from you. The banks killing it focus on both digital AND actual humans - like, don't make me wait forever on hold but also don't make everything so robotic. Response times and actually solving problems matter way more than fancy marketing. Oh, and stop making every interaction feel like a transaction!

Honestly? It's mostly old tech and people being stubborn about change. Most banks are still running on mainframes from like the 80s that somehow need to work with modern stuff - which is actually pretty wild that it even functions. But then you've also got employees and managers who just don't want to learn new systems. Plus banking regulations mean you can't just wing it and hope nothing breaks, since it's actual people's money. The key thing is you need to focus just as much on getting people on board and slowly upgrading systems as you do on the tech itself.

Honestly, just pick one high-volume thing you do over and over - like opening accounts or processing loans - and automate that first. Map out your current workflow, find where stuff gets stuck, then fix those bottlenecks. I've watched banks slash their processing time by 40% doing exactly this. Digital workflows are total game-changers for customer onboarding too. Oh, and definitely consolidate your back-office systems if you can - so much redundant crap gets eliminated. AI works great for document verification and risk stuff. Measure where you're at now, then optimize from there. Straight-through processing should be your goal wherever possible.

Honestly, your biggest wins are gonna come from making banking feel more like Netflix or Instagram - you know, actually intuitive. People want everything instant and available whenever. What's wild is younger customers are actually hungry for financial education now, which nobody saw coming. They're also way more into automated savings and wellness tools than before. Green banking products are having a moment too with the whole sustainability push. Focus on nailing those smooth digital experiences first. Then bundle some financial coaching with your regular services - that combo is where you'll crush the competition right now.

Ugh, regulatory changes are such a pain - they basically make you drop everything and scramble to meet new rules. Like when Basel III hit, banks had to pull resources from growth projects just to stay compliant. Your long-term planning gets totally derailed. The smart banks though? They actually build flexibility into their strategy upfront. Always keep some buffer room when you're planning big moves, and honestly, staying on top of policy news isn't optional anymore. Makes the whole process way less chaotic when changes do come down the pipeline.

Dude, fintech companies are literally crushing traditional banks right now. They're faster, cheaper, and way more user-friendly - stuff like Venmo for payments, P2P lending platforms, robo-advisors for investing. The crazy part? They don't deal with all the regulatory red tape and ancient computer systems that slow banks down. So they can pivot quickly and offer better rates. Younger people especially trust these apps more than walking into some marble-columned bank branch. Honestly, banks either need to team up with these companies or completely overhaul their digital presence. Otherwise they're toast.

Honestly, you've gotta meet them on their phones - that's where they live. Mobile experience needs to be flawless, with instant transaction alerts and AI that actually gives useful financial insights. Gamification is clutch here - savings challenges, spending streaks, that kind of stuff really hooks them. They're way more into social responsibility than older generations, so definitely push your ESG stuff and sustainable investing options. Oh, and make it feel less like traditional banking, more like their favorite social app. I'd start by getting some Gen Z folks on your team to roast your current platform - they'll tell you exactly what sucks about it.

Look, economic stuff totally controls your whole SWOT analysis in retail banking. Strong economy? You'll see more loan demand and people depositing cash left and right. Recessions though - that's when defaults spike and profits tank. Interest rates mess with your margins big time too. Growth periods can actually expose weak risk management if you're not careful during expansion. Honestly, banks that don't plan for different scenarios always get blindsided. You should definitely run your SWOT through various economic what-ifs before making any major moves.

Honestly, you'll want to layer your defenses - good encryption and multi-factor authentication are must-haves. Train your employees too because people clicking random links is still the

-

Excellent design and quick turnaround.

-

Happy to found you SlideTeam. You guys are value for money. Amazing slides.