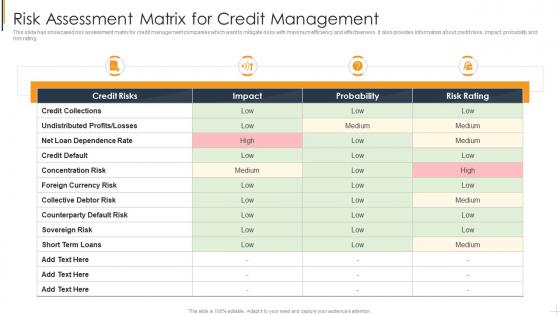

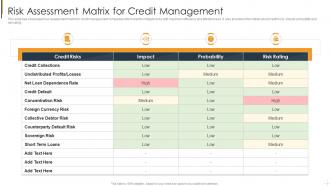

Risk Assessment Matrix For Credit Management

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

This slide has showcased risk assessment matrix for credit management companies which want to mitigate risks with maximum efficiency and effectiveness. It also provides information about credit risks, impact, probability and risk rating

People who downloaded this PowerPoint presentation also viewed the following :

Risk Assessment Matrix For Credit Management with all 6 slides:

Use our Risk Assessment Matrix For Credit Management to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Risk Assessment Matrix

Primary factors influencing credit risk assessment include borrower's credit history, income stability, debt-to-income ratio, collateral value, and employment duration. These elements enable financial institutions to streamline loan approvals, minimize default rates, and enhance portfolio performance, with banks and credit unions increasingly finding that comprehensive assessment delivers better risk management and competitive lending advantages.

Credit score significantly impacts credit risk evaluation by serving as a primary indicator of borrower reliability, repayment history, and default probability. Financial institutions use credit scores alongside income verification, debt-to-income ratios, and collateral assessment to streamline lending decisions, with many banks finding that higher credit scores correlate with lower default rates, ultimately enabling faster loan approvals and competitive interest rate offerings.

Economic indicators serve as crucial predictors in credit risk assessment, including GDP growth rates, unemployment levels, inflation rates, interest rate trends, and industry-specific metrics. These indicators help financial institutions evaluate borrowers' ability to repay during varying economic conditions, with many banks finding that incorporating macroeconomic data significantly enhances their risk models and reduces default rates.

Machine learning algorithms enhance traditional credit risk assessment by analyzing vast datasets, identifying complex patterns, and providing real-time risk evaluations that static models cannot achieve. Through advanced predictive analytics, banks and financial institutions streamline loan approvals, minimize default rates, and deliver faster customer experiences, while ultimately reducing operational costs and maintaining competitive advantage in increasingly dynamic markets.

Corporate credit risk assessment evaluates business financial statements, cash flows, industry conditions, management quality, and debt structures, while consumer credit risk focuses on personal income, credit history, debt-to-income ratios, and spending patterns. These approaches differ significantly in complexity and data sources, with corporate assessments requiring deeper financial analysis and industry expertise, while consumer evaluations rely heavily on credit scores and standardized metrics, ultimately enabling lenders to make informed decisions across different market segments.

Macroeconomic trends significantly impact credit risk across industries through interest rate fluctuations, inflation cycles, employment levels, and GDP growth patterns. Industries like retail and hospitality face heightened risk during economic downturns, while healthcare and utilities remain more resilient, with many financial institutions finding that diversified portfolios and sector-specific analysis ultimately deliver more accurate risk assessments.

Best practices for conducting due diligence in credit risk assessment include comprehensive financial statement analysis, cash flow evaluation, collateral verification, industry trend assessment, and borrower credit history review. These methodologies enhance decision-making by identifying potential red flags, quantifying exposure levels, and establishing appropriate risk pricing, with many financial institutions finding that systematic due diligence processes reduce default rates while accelerating loan approval timelines.

Regulatory frameworks significantly influence credit risk assessment by mandating specific capital requirements, standardizing risk measurement methodologies, and enforcing comprehensive reporting protocols. These regulations, including Basel III and Dodd-Frank, compel banks and financial institutions to adopt more rigorous stress testing, enhanced data governance, and transparent risk disclosure practices, ultimately delivering improved financial stability and stronger consumer protection across the industry.

Essential data for accurate credit risk analysis includes financial statements, credit history, employment records, debt-to-income ratios, and collateral valuations. These data sources work together by providing comprehensive borrower profiles, enabling real-time risk scoring, and supporting automated decision-making, with many financial institutions finding that integrated data analytics ultimately delivers faster loan approvals and significantly reduced default rates.

Credit risk assessment integrates into underwriting processes through automated data analysis, real-time credit scoring algorithms, and seamless API connections with existing loan management systems. These technologies enable banks and financial institutions to accelerate loan approvals, reduce manual review time, and enhance decision accuracy, while maintaining comprehensive risk evaluation standards that ultimately deliver faster customer service and improved operational efficiency.

Assessing credit risk for startups presents challenges including limited financial history, unproven business models, volatile cash flows, lack of collateral, and higher uncertainty compared to established businesses with extensive track records. While established companies offer predictable revenue patterns and comprehensive financial data, startups require alternative evaluation methods focusing on market potential, management expertise, and innovative scoring models, ultimately demanding more nuanced risk assessment approaches.

Behavioral data enhances credit risk assessment by analyzing spending patterns, transaction frequency, account management habits, and payment timing beyond traditional credit scores. This comprehensive approach enables lenders to identify creditworthy borrowers who might be overlooked by conventional metrics, while detecting potential risks through inconsistent behaviors, ultimately delivering more accurate lending decisions and expanded financial inclusion.

Misjudging credit risk leads to significant financial losses, increased default rates, regulatory penalties, and damaged institutional reputation. Banks and financial institutions face reduced profitability, stricter oversight requirements, and potential capital adequacy issues, while borrowers experience limited access to future credit, ultimately undermining market confidence and competitive positioning.

Geopolitical risks significantly impact credit risk assessment by influencing borrower stability, market volatility, currency fluctuations, and regulatory changes across regions. Financial institutions analyze political tensions, trade disputes, sanctions, and government policy shifts when evaluating creditworthiness, with many banks incorporating geopolitical risk models to enhance portfolio management and minimize exposure to politically unstable markets.

Financial institutions can leverage machine learning algorithms, automated credit scoring systems, alternative data analytics platforms, real-time monitoring tools, and integrated risk management software to automate credit risk assessment. These technologies streamline decision-making by analyzing vast datasets, reducing processing times, and enhancing accuracy, with many banks finding that automated systems deliver faster loan approvals while significantly minimizing default risks.

-

The design is very attractive, informative, and eye-catching, with bold colors that stand out against all the basic presentation templates.

-

You guys are life-saver when it comes to presentations. Honestly I cannot do much without your services. Thank you!!!