Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Credit risk management reduces losses by determining the adequacy of a banks capital and loan loss reserves at any given time. This process has long been difficult for financial institutions to master. Our Credit Risk Management Frameworks for Banks presentation helps to establish an appropriate credit risk environment, maintaining an appropriate credit administration, measurement, and monitoring process. This credit risk management presentation includes various slides related to current analysis details such as key figures related to the bank, worldwide presence and alliances of the bank, market share and turnover related to the competitors, etc. It showcases the various problems associated with credit risk management with their primary causes. It also focuses on risks in the banking industry, principal risks components and ley parameters, data analysis on bank NPAs, etc. Also, this presentation covers slides for credit risk analysis, techniques for managing and mitigating various credit risks, technologies used to manage credit risks, etc. The module also concentrates on the credit rating process from issues and rating agencies, maintaining appropriate credit administration, setting up of credit management system, etc. In the end, it shows the positive effects of implementing the credit risk strategy on the company, such as a decrease in non-performing loans and credit risk recovery management details. Get access now.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

Slide 1: This slide introduces Credit Risk Management Frameworks for Banks. State your company name and begin.

Slide 2: This slide states Agenda of the presentation.

Slide 3: This slide shows Table of Content for the presentation.

Slide 4: This slide highlights title for topics that are to be covered next in the template.

Slide 5: This slide presents Key Figures Related to the Bank.

Slide 6: This slide displays Worldwide Presence and Alliances of the Bank.

Slide 7: This slide represents Market Share and Turnover Related to the Competitors.

Slide 8: This slide highlights title for topics that are to be covered next in the template.

Slide 9: This slide showcases Challenges to Credit Risk Management.

Slide 10: This slide shows Primary Causes of Credit Risks.

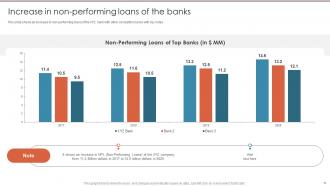

Slide 11: This slide presents Increase in Non-Performing Loans of the Banks.

Slide 12: This slide displays Risks in Banking: New Matters Arising.

Slide 13: This slide highlights title for topics that are to be covered next in the template.

Slide 14: This slide represents Principal Risks Components and Key Parameters.

Slide 15: This slide showcases Data Analysis on Bank NPA’s.

Slide 16: This slide shows Benefits of Credit Risk Management for the Bank.

Slide 17: This slide highlights title for topics that are to be covered next in the template.

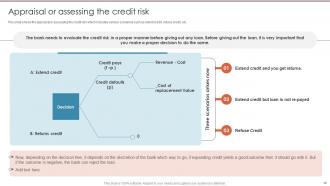

Slide 18: This slide presents Appraisal or Assessing the Credit Risk.

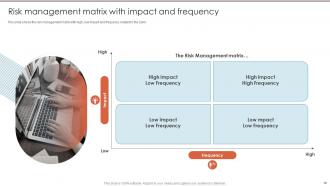

Slide 19: This slide displays Risk Management Matrix with Impact and Frequency.

Slide 20: This slide highlights title for topics that are to be covered next in the template.

Slide 21: This slide represents Effective Measure to Manage Credit Risk.

Slide 22: This slide showcases Credit Risk Analysis Related to the Bank.

Slide 23: This slide shows Managing and Mitigating Credit Risk by Various Credit Risk Management Techniques.

Slide 24: This slide presents Mitigating Credit and Control of Risks.

Slide 25: This slide displays Using Technologies To Manage Credit Risk.

Slide 26: This slide highlights title for topics that are to be covered next in the template.

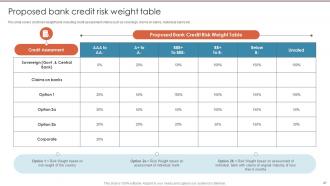

Slide 27: This slide represents Proposed Bank Credit Risk Weight Table..

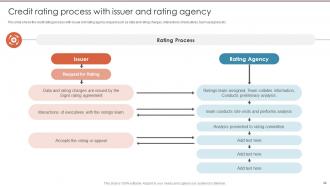

Slide 28: This slide showcases Credit Rating Process with Issuer and Rating Agency.

Slide 29: This slide shows Maintaining Appropriate Credit Administration, Measurement And Monitoring Process.

Slide 30: This slide presents Setting Up of Bank Credit Risk Management System.

Slide 31: This slide highlights title for topics that are to be covered next in the template.

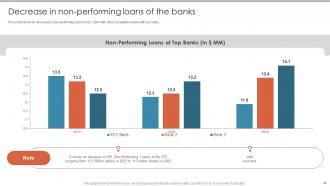

Slide 32: This slide displays Decrease in Non-Performing Loans of the Banks.

Slide 33: This slide represents Credit Risk Recovery Management Details.

Slide 34: This slide contains all the icons used in this presentation.

Slide 35: This slide is titled as Additional Slides for moving forward.

Slide 36: This is About Us slide to show company specifications etc.

Slide 37: This is Our Mission slide with related imagery and text.

Slide 38: This slide presents Bar chart with two products comparison.

Slide 39: This slide shows Post It Notes. Post your important notes here.

Slide 40: This slide displays Bar chart with two products comparison.

Slide 41: This slide contains Puzzle with related icons and text.

Slide 42: This slide depicts Venn diagram with text boxes.

Slide 43: This is a Thank You slide with address, contact numbers and email address.

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides with all 48 slides:

Use our Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

-

Credit Risk Management Frameworks For Banks Powerpoint Presentation Slides

FAQs for Credit Risk Management Frameworks For Banks

You'll want solid credit policies first - those set your lending standards. Then build out risk assessment processes and monitoring systems that actually work. Set up approval workflows with clear limits too. Someone has to watch this stuff though, so governance oversight is huge. Early warning systems are clutch for catching problems before they blow up. Also need collection procedures ready when loans go bad (and they will). The tricky part? Making sure it all connects properly so nothing gets missed. I'd honestly just map what you're doing now and fix the worst gaps first.

So regulatory requirements are basically your foundation - you can't just ignore them and build whatever you want. Basel III and similar regs tell you exactly what your capital ratios need to be, how to run stress tests, all that fun stuff. I know it sounds like a nightmare at first, but honestly? Regulators already did the heavy lifting by mapping out minimum standards for risk measurement and reporting. You've gotta hit those benchmarks before adding your own business-specific tweaks. Start with an audit of what you have now versus current guidelines. That'll show you where the gaps are.

Dude, machine learning is seriously changing everything with credit risk. These algorithms can crunch through tons of data and catch patterns we'd totally miss. Way more accurate than old-school scoring methods too. The automated processing is clutch - faster decisions, less human bias screwing things up. Oh, and you get real-time monitoring so you can actually see how your portfolio's doing as things change. Honestly started getting excited about this stuff once I saw the results firsthand. I'd say start with automated data collection first since that's gonna be your base for everything else.

Look, start with your solid numbers - credit scores, debt ratios, cash flow stuff. Then add the softer judgment calls on top. Most teams I know use scoring systems that weight both types of data, or they'll set up triggers where bad numbers automatically kick off a deeper dive into management quality, industry stuff, relationship history. Honestly, the biggest mistake is treating qualitative factors like an afterthought. You need clear rules for when gut feelings can overrule the spreadsheet - otherwise you're just wasting time collecting insights you won't actually use.

Honestly, when everything's going sideways, diversification becomes your best friend. Don't dump everything into one sector or region - even if it seemed bulletproof before. I'd bump up your monitoring from quarterly to monthly, maybe weekly for the sketchy accounts. Tighten up collateral requirements too, and think about shorter payment terms for new clients. Markets change fast these days. Your old thresholds might be useless now, so stay flexible and don't be afraid to pull back hard when you see red flags. Better safe than sorry, right?

So big companies have these crazy formal credit committees and scoring models - like dedicated risk teams in every region. Small businesses? Owner just runs a quick credit check and goes with their gut, which honestly works fine when you actually know your customers. The corporates need all that complex stuff because they're juggling thousands of clients plus regulatory headaches. Meanwhile small biz keeps it straightforward with basic credit limits. Oh, and if you're growing - build those formal processes early. Trust me on that one.

Ugh, data quality is your biggest headache - counterparty info gets scattered across different systems, so you never see the full picture. Correlations are tricky too. Everything looks fine until markets tank and you realize all your "independent" counterparties actually share the same funding sources. It's like dominoes falling. Real-time updates are nearly impossible, and don't even get me started on measuring indirect exposures. That stuff gets messy fast. I'd start by figuring out where your data lives and mapping those hidden relationships between counterparties. Trust me, the blind spots will surprise you.

Honestly, your credit models need to get smarter about what's coming, not just what happened. Traditional metrics are fine but you're missing tons of data - social media vibes, ESG stuff, real-time transactions. ML can spot patterns way faster than old-school methods. The downside? Regulators get nervous about black box algorithms, which I totally get. You can work around this with explainable AI and stress tests that factor in climate risks, cyber attacks, geopolitical mess. My advice: figure out what risks actually threaten your portfolio first, then slowly test new data sources instead of going all-in.

Start with PD, LGD, and EAD - those are your bread and butter for expected loss calcs. Credit scores are obvious, but debt-to-income and LTV ratios matter tons too depending on the loan type. Portfolio stuff gets trickier with concentration risk metrics. Most places I've seen track delinquency and charge-offs as well, though those lag behind obviously. Honestly once you get the big three down, everything else just clicks into place. Oh and if you're doing any consumer lending, payment history patterns are gold - way more predictive than people think.

Risk appetite is basically your "risk budget" - it sets the boundaries for how much risk you're cool with taking to hit your goals. This flows into everything: lending criteria, who you'll work with, pricing models, concentration limits. Without it, you're just making stuff up as you go (spoiler alert: that's a terrible idea). The key thing though? Don't let it become some fluffy executive document that sits in a drawer. Your team needs concrete policies and thresholds they can actually use day-to-day.

Look, credit scoring models are basically the backbone of your whole risk setup. They automate decisions and give you solid, data-driven ways to evaluate borrowers instead of just going with your gut (which can be pretty inconsistent, let's be honest). You can process tons of applications efficiently while keeping your risk standards intact. They help you figure out default probability, set pricing, determine credit limits - the whole deal. Just make sure you're actually tracking how well they're performing and updating them regularly. Otherwise you'll end up with models that worked great in 2019 but are totally off now.

Run them quarterly minimum - I'd use both historical stuff like 2008 and made-up future scenarios. Model how your whole portfolio tanks during economic crashes, sector meltdowns, interest rate jumps, whatever. Most teams barely do this though, which is nuts. Test individual loans AND the full portfolio, then actually change your risk limits based on what you find. Don't just stick the reports in a drawer somewhere! The whole point is using those results to tighten up lending standards before everything goes sideways. Oh and do both loan-level and portfolio-level analysis - you need both perspectives.

Set up daily risk dashboards tracking your main stuff - portfolio concentration, delinquency rates, sector exposure limits. Don't wait for monthly reports like some teams do. That's how you get screwed when things move fast. Real-time monitoring saves your ass. Include forward-looking indicators too, not just what already happened. Stress test results, early warning signals - that kind of thing. You need clear triggers that auto-flag when thresholds get breached. Honestly, just pick your top 10 risk indicators first and build everything around those.

Honestly, culture can totally tank your credit risk setup if you're not careful. When people are just chasing sales numbers, they'll skip proper checks or ignore obvious warning signs. You need folks to feel comfortable speaking up about sketchy deals without getting steamrolled by the sales team - which is harder than it sounds, trust me. Leadership sets the tone here. If the executives blow off risk rules, everyone else will follow suit. Bottom line? Your bonus structure can't just reward revenue. Celebrate the people who actually catch problems before they blow up in your face.

Honestly, the credit risk game is changing fast right now. AI isn't optional anymore - everyone's using it for real-time assessments and predictive stuff. ESG factors are suddenly part of credit decisions too, which blindsided a lot of banks if I'm being real. Instead of those old quarterly reviews, it's all about continuous monitoring now. Regulators want everything integrated across risk types. Oh, and get your data infrastructure sorted ASAP because literally all of this depends on having clean data flows. That's probably the most important thing you can do right now.

-

I was able to find the right choice of PPT template for my thesis with SlideTeam. Thank you for existing.

-

SlideTeam never fails to surprise me with its amazing PPT designs. Thanks team for providing me with your constant support!