Credit scorecard powerpoint presentation slides

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Credit scorecards determine the interest rates you pay on loans, are used to premium for homeowners coverage, check your reliability for paying off debt, etc. Here is a professionally designed template on a Credit Scorecard that will assess the risk of an individual and asset and provide details of income and status. Using a compliance matrix, a company can demonstrate its key parameters like history scorecard, new customer applying for a loan, etc. The proposal displays the individual credit rating scorecard, customer credit scores, etc. The products have a breakdown for costs as each element carries equal weightage in deciding the value for credit. The proposal includes the minutest details of the timeline for each credit score. Highlights are there for emphasis on score analysis metrics, credit metrics, credit barometers, etc. The scorecard displays the details regarding customers credit scores, score ratings, and more. The format underlines the critical points of the credit. Get access to our 100 percent editable Scorecard template and download it now.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

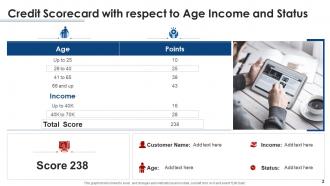

Slide 1: This slide introduces Credit Scorecard with respect to Age Income and Status. State Your Company Name and begin.

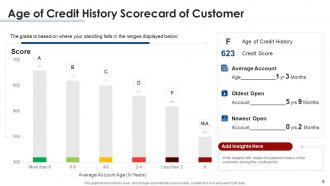

Slide 2: This slide shows Age of Credit History Scorecard of Customer.

Slide 3: This slide presents Credit Scorecard of new Customer Applying for Loan.

Slide 4: This slide shows Individual Credit Rating Scorecard in comparison with Previous Years.

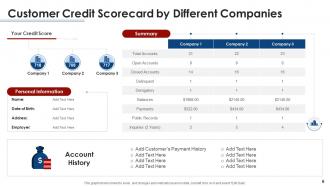

Slide 5: This slide displays Customer Credit Scorecard by Different Companies.

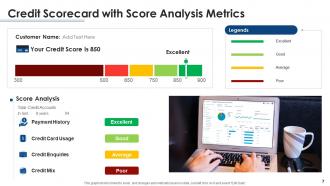

Slide 6: This slide represents Credit Scorecard with Score Analysis Metrics.

Slide 7: This slide shows Credit Scorecard Ratings with key Metrics.

Slide 8: This slide presents Credit Scorecard Barometer with Ratings.

Slide 9: This slide shows Key Metrics to measure Credit Scorecard of Consumer.

Slide 10: This slide displays Credit Scorecard Ratings with key Influential Factors.

Slide 11: This slide represents Icons for Credit Scorecard.

Slide 12: This slide is titled as Additional Slides for moving forward.

Slide 13: This slide presents 30 60 90 Days Plan with text boxes.

Slide 14: This slide shows Roadmap with additional textboxes.

Slide 15: This is a Financial slide. Show your finance related stuff here.

Slide 16: This is a Timeline slide. Show data related to time intervals here.

Slide 17: This slide shows Venn diagram with text boxes.

Slide 18: This slide presents Post It Notes. Post your important notes here.

Slide 19: This is a Comparison slide to state comparison between commodities, entities etc.

Slide 20: This slide displays Stacked Bar chart with two products comparison.

Slide 21: This slide represents Column chart with two products comparison.

Slide 22: This is a Thank You slide with address, contact numbers and email address.

Credit scorecard powerpoint presentation slides with all 28 slides:

Use our Credit Scorecard Powerpoint Presentation Slides to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Credit scorecard

So credit scores break down into a few key things. Payment history is huge - like 35% of the whole thing, so don't miss payments if you can help it. Credit utilization matters too (that's how much of your limit you're using). Your credit history length counts, plus what types of accounts you have. New inquiries affect it but honestly not as much as everyone freaks out about. I'd focus on paying on time and keeping your balances low if you want to see changes fast. Those two will give you the biggest bang for your buck.

Yeah, every lender basically builds their own scorecard based on who they usually lend to. Banks love steady income above everything else. Credit unions? They're more about your history with them as a member. Fintech companies are doing some crazy stuff now - like looking at your app usage or social media (kinda creepy if you ask me). Traditional banks stick to the boring basics: payment history, how much debt you've got. Don't get discouraged if one place says no though. Their models are totally different, so you might have better luck somewhere else.

So credit scores are basically lenders' cheat sheet for figuring out if you'll pay them back. They take your payment history, how much debt you're carrying, how long you've had credit - all that stuff - and turn it into one number. Way better than the old days when loan officers just went with their gut, honestly. Higher score means you're less risky, which gets you better interest rates. It's pretty straightforward but makes a huge difference when you're trying to get a mortgage or whatever. Your score literally determines what you qualify for and how much it'll cost you.

Honestly, just focus on paying bills on time - that's like 35% of your score right there. Keep credit card balances super low, maybe 10% of your limit if you can swing it. I learned this the hard way, but don't close old cards even if you're not using them anymore. Your credit history length actually matters. Also avoid opening a bunch of new accounts at once because that looks sketchy to lenders. Having different types of credit helps too - cards, maybe a car loan, whatever. It takes a few months to see changes, so don't expect overnight miracles.

Honestly, don't stress about it too much. Hard inquiries only ding your score like 5-10 points and it's temporary anyway. Soft ones (like when you check your own score) don't even count. Here's the thing though - if you're shopping for a car loan or mortgage, multiple inquiries within a couple weeks usually just count as one. Pretty smart system actually. The hit basically disappears after a year, and they fall off completely after two. I used to worry about this stuff way more than I needed to. Just don't go crazy applying for credit cards every month and you'll be fine.

So basically your credit score works like a weighted average - some stuff matters way more than others. Payment history is huge, like 35% of your score, so missed payments will absolutely wreck you. Credit utilization is almost as important at 30%. I always thought that one was weird but apparently keeping your balances low is critical. The other factors - how long you've had credit, new inquiries, credit mix - they matter but not nearly as much. My advice? Don't stress about the small stuff. Just pay your bills on time and keep those credit card balances low. That's like 65% of your score right there.

Logistic regression is probably your best bet starting out - it's what FICO still uses and regulators actually understand it. Decision trees and random forests are pretty common too. Honestly, a lot of fintech companies are playing with gradient boosting and neural networks now, but good luck explaining those to compliance lol. Weight of Evidence scorecards are another option if your risk team needs something super interpretable. There's always that accuracy vs explainability trade-off though. I'd mess around with ensemble methods later if you need the performance boost, but logistic regression covers most regulatory boxes and actually makes sense when you're presenting results.

Check your credit score every 3 months minimum - monthly's even better if you're trying to fix it. I used to be lazy about this and only looked twice a year. Terrible idea. Random errors show up all the time, and if you catch them fast you can dispute before they tank your score. Also helps you spot if someone's using your info for sketchy stuff. Oh, and you'll actually see whether paying off that credit card or whatever is helping. Definitely set a phone reminder though because I always forgot otherwise.

Ugh, late payments are brutal for your credit. Payment history is like 35% of your score, so missing payments really messes things up. One 30-day late payment? That can tank your score by 60-110 points depending where you started. Honestly, it's kind of ridiculous how harsh they are about it. The damage sticks around for 7 years too, though it hurts less as time goes on. Recent late payments are way worse than old ones. My advice? Set up autopay for at least the minimums so you don't accidentally screw yourself over again.

So basically credit scorecards let you set automatic approval cutoffs and catch risky applicants early. They turn stuff like payment history, debt ratios, and income into actual numbers instead of just going with your gut - which honestly makes way more decisions. You'll need to update the scorecard regularly with new data and tweak those cutoff scores based on how many people actually default. Oh, and definitely look at your current customers first to figure out what warning signs matter most for your specific business.

Dude, credit scoring is getting wild right now. Lenders aren't just looking at your payment history anymore - they're pulling data from everywhere. Social media, utility bills, even how you use your phone. It's honestly kind of creepy but also opens doors for people with thin credit files. Cloud tech means they can update these models constantly instead of once a year, which is huge. The tricky part? Regulators still want explanations for decisions, so companies are using AI that can actually show its work. These new scorecards basically learn and adjust themselves automatically.

So credit companies basically split people into different groups when scoring them. A 22-year-old college grad isn't gonna have the same spending patterns as someone in their 40s with a mortgage, you know? They create separate models based on stuff like income, where you live, how long you've had credit. Young people might get dinged less for having short credit history but more weight on whether they actually pay on time. It's honestly pretty smart. Just gotta make sure you're testing across all groups so you don't accidentally screw over certain demographics.

Honestly, the fairness stuff is gonna be your biggest headache. Can't use anything that ties back to race, gender, age - even if it seems predictive (spoiler: some definitely will). Your model might pick up on zip codes or income patterns that basically discriminate without saying it outright. Transparency's tricky too - people want to know how you're scoring them, but you can't just hand over your secret sauce. I'd say get different people reviewing your models before launch. Oh, and build in bias testing from day one, not as an afterthought.

So predictive analytics is pretty much a game-changer for credit scoring. You're pulling in way more data than just the usual stuff - like spending patterns, seasonal changes, even social media behavior (which honestly feels a bit creepy but whatever). Machine learning keeps getting better as it processes new info, so you catch risky borrowers faster. The cool part? Way fewer mistakes on approvals and rejections. Your loan decisions improve and customers aren't as pissed off. I'd start by figuring out what alternative data you can actually get your hands on first.

Just go straight to whichever credit bureau sent you the scorecard - Experian, Equifax, or TransUnion. Online's your best bet since it's way faster than calling or mailing stuff. Tell them exactly what's wrong and attach any proof you've got. They have to get back to you within 30 days, and if they find the mistake, they'll fix your report and send an updated scorecard. Oh, and if the same error shows up on reports from different bureaus, you'll need to dispute it with each one separately - they're weirdly bad at talking to each other about corrections.

-

It saves your time and decrease your efforts in half.

-

Use of icon with content is very relateable, informative and appealing.