Credit Unions Powerpoint Presentation Slides

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Give an overview of banking by using our content ready credit union PowerPoint presentation slides. The ready to use commercial banks presentation deck comprises 42 slides which covers various important topics like US banking structure, banking organizational hierarchy, income statement, balance sheet, banking industry overview, major trend in the US banking industry, leading US banks in revenue, key growth drivers in the US banking industry, federal bank regulation in the US and many other slides. Talk about banking facilities & services with the help of our financial cooperative PowerPoint template. Give clarity to your clients on different types of loans offered like an auto loan, housing loan, equity loan, personal loan, credit loan using our banking PowerPoint theme. Understand the SWOT analysis, banking environment PESTEL analysis, Porter’s five forces model by using our visually appealing and professionally designed financial cooperative PPT slides. Get them to genuinely care for each other with our Credit Unions Powerpoint Presentation Slides. They build greater family bonds.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

Slide 1: This slide introduces Credit Unions. State Your Company Name and begin.

Slide 2: This slide shows Content of the presentation.

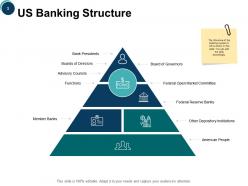

Slide 3: This slide presents US Banking Structure with related diagram.

Slide 4: This slide displays Banking Organizational Hierarchy with designations.

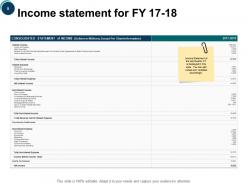

Slide 5: This slide represents Income statement for FY 17-18. You can add values and variables accordingly.

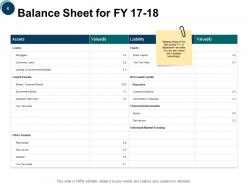

Slide 6: This slide showcases Balance Sheet for FY 17-18.

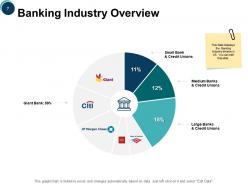

Slide 7: This slide shows Banking Industry Overview with the help of donut pie chart.

Slide 8: This slide presents Key US Banking Industry Statistics.

Slide 9: This slide displays Major Trends in US Banking Industry.

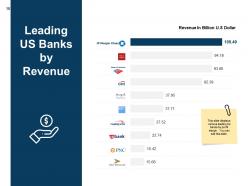

Slide 10: This slide represents Leading US Banks by Revenue in graphical form.

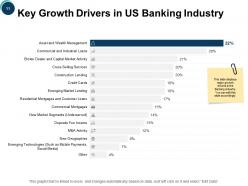

Slide 11: This slide showcases Key Growth Drivers in US Banking Industry.

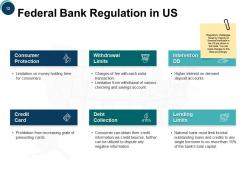

Slide 12: This slide shows Federal Bank Regulation in US describing- Credit Card, Debt Collection, Lending Limits, Interest on DD, Consumer Protection, Withdrawal Limits.

Slide 13: This slide displays various services provided by banks to its customers.

Slide 14: This slide presents wide range of Loan Categories.

Slide 15: This slide represents Types of Loan including- Auto Loan, Housing Loan, Equity Loan, P2P Lending, Small Medium Businesses Loan, Payday Lending, Personal Loan, Credit Loan.

Slide 16: This slide showcases Domestic Locations of different bank branches.

Slide 17: This slide shows Overseas Location of banks with map.

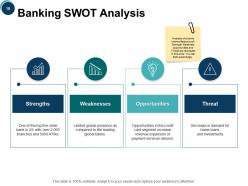

Slide 18: This slide presents Banking SWOT Analysis describing- Weaknesses, Threats, Opportunities, Strengths.

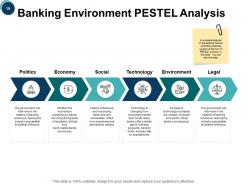

Slide 19: This slide displays Banking Environment PESTEL Analysis describing- Politics, Economy, Social, Technology, Environment, Legal.

Slide 20: This slide represents Porter’s Five Forces Model as New Entrants, Threat form substitutes, Bargaining power of suppliers, Rivalry among current players, Bargaining power of customers.

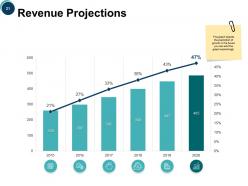

Slide 21: This slide showcases Revenue Projections in graphical form.

Slide 22: This slide displays Credit Unions Icons.

Slide 23: This slide reminds about a 15 minutes coffee break.

Slide 24: This slide shows Area Chart with three products comparison.

Slide 25: This slide showcases Clustered Column-Line to compare different products.

Slide 26: This slide displays Donut Pie Chart with data in percentage.

Slide 27: This slide presents Clustered Bar chart with three products comparison.

Slide 28: This slide is titled as Additional Slides for moving forward.

Slide 29: This is Our Mission slide with related icons and text boxes.

Slide 30: This is About Us slide to show company specifications.

Slide 31: This is Our Team slide with names and designation.

Slide 32: This is a Comparison slide to state comparison between commodities, entities etc.

Slide 33: This is a Financial slide. Show your finance related stuff here.

Slide 34: This is a Quotes slide to convey message, beliefs etc.

Slide 35: This is a Timeline slide to show information related with time period.

Slide 36: This is another slide continuing Timeline.

Slide 37: This slide is titled as Post It Notes. Post your important notes here.

Slide 38: This is a Lego slide with additional text boxes.

Slide 39: This is a Venn slide with text boxes to show information.

Slide 40: This slide shows Dashboard with text boxes. Show relevant information accordingly.

Slide 41: This is a Target slide. State your targets here.

Slide 42: This is a Thank You slide with address, contact numbers and email address.

Credit Unions Powerpoint Presentation Slides with all 42 slides:

Control the extent of damage with our Credit Unions Powerpoint Presentation Slides. Effectively bring down the amount of destruction.

FAQs for Credit Unions

Credit unions are member-owned, so you actually get a vote in decisions instead of some random shareholders calling the shots. Way better rates on loans and savings too since they're not trying to squeeze every penny out of you. The catch? You need to qualify for membership - usually through work, where you live, or being part of some group. Banks have tons more locations though, which is super convenient when you're traveling or whatever. But honestly, if you can get into a credit union, the customer service is so much better and fees are way lower. Does your work have a credit union partnership? Worth checking out.

So credit unions basically look at the federal funds rate, their own costs, and what they need to stay afloat. But here's the thing - they're member-owned, not trying to make shareholders rich like regular banks. That means you'll usually get better savings rates and cheaper loans. They also check out what other local places are offering. Honestly, I've always had better luck with credit unions than big banks - way less annoying fees too. You should call around to a few in your area and compare rates. They're usually pretty upfront about their numbers.

Honestly, credit unions are pretty great - way better rates since they're not trying to squeeze profit from you like regular banks. Your savings actually earn decent interest, and loan rates don't suck. Customer service is legit personal too, not some call center nightmare. They're way more chill about lending if your credit's kinda meh. Only downside? Not as many locations or ATMs, which can be annoying when you're traveling. Check if you qualify through your job or maybe family - sometimes the requirements are random but worth it.

So credit unions are member-owned, which is pretty sweet because they put profits back into helping people instead of making rich shareholders richer. Lower loan rates, better savings rates, way fewer annoying fees than regular banks. They do tons of local stuff too - like financial classes, small business loans, scholarships for kids in the area. You actually get voting rights since you're technically an owner. Customer service is genuinely better, not that fake corporate BS. My cousin switched to one last year and loves it. Definitely worth looking into if you want banking that doesn't suck.

So credit unions have this board of directors that members vote for - they're the ones making all the big calls. They hire the CEO, decide loan policies, set what you earn on savings, that whole thing. Pretty different from regular banks where it's all about shareholders getting rich. Your board actually has to answer to you since you're technically an owner. Oh and here's something cool - most let you show up to their meetings if you're curious. You could even run for a spot yourself, though honestly that sounds like way more work than I'd want to deal with.

Honestly, credit unions have gotten way better at tech stuff lately. Most have decent mobile apps now with check deposit and budgeting tools. Real-time alerts too, which is nice. They're doing chatbots for basic questions, and some even have AI that gives you financial advice - though I'm still not totally sold on that part. Online loan applications are standard now, thank god, because the old paper process was awful. Here's the thing though - they're actually faster at adopting new fintech partnerships than big banks since they don't have all that ancient infrastructure holding them back. Definitely test their app before switching.

So you'll need to qualify first - could be through work, where you live, or even family ties. Some credit unions are super strict about this, others not so much. Fill out their application and you'll have to open a share savings account with like $5-25. Pretty low barrier honestly. Basic stuff like ID and personal info required. Once you're approved, congrats - you're actually a member-owner with voting rights and everything. I'd start by googling which ones you can join or just ask HR if your company has one. Way easier than I thought it'd be when I first looked into it.

Your money's pretty safe with credit unions, honestly. They've got NCUA insurance that covers up to $250k just like regular banks do. The big difference? They're owned by members, not shareholders trying to squeeze every penny out. So they don't take crazy risks with your cash. Most have solid capital reserves too. I actually think their community-focused approach makes them way more stable - they know their borrowers personally, which keeps default rates low. Oh, and there's tons of regulatory oversight keeping them in check. You can always look up your credit union's financial ratings online if you're worried.

So credit unions are actually pretty solid - way better rates on savings and cheaper loans since they're not trying to squeeze profit from you. Auto loans, mortgages, personal loans, all that stuff is usually better. Free checking is common too, which banks love to charge for now. Some even do financial counseling or give members dividends at year-end, which is cool. Only thing is you gotta qualify for membership first - each one has different rules about who can join. But honestly? Big banks feel so greedy compared to credit unions.

So credit unions are actually perfect for this since they're member-owned and don't have shareholders breathing down their necks. They can offer basic accounts with way lower fees and be more flexible with lending - like not punishing someone for spotty income or thin credit. Building trust is huge though. Partner with local community groups, offer stuff in different languages, meet people where they actually are financially instead of lecturing them. Oh and financial education programs help too, but make them actually relevant to people's real situations. Big banks basically ignore these folks, so there's definitely an opportunity there.

So credit unions have this "field of membership" thing where you need some connection to join. Could be your job, where you live, your church, school - whatever. Some are super specific to certain companies or industries, others just cover whole areas. Oh and if your family's already in one, you can usually get in too which is handy. Honestly the rules are all over the place depending on which one you're looking at. I'd just google credit unions near you and check out their membership requirements. Most have it right on their websites.

So your credit union's board and loan committee basically hash out the lending rules together. They look at all the usual stuff - credit scores, how much debt you already have, what kind of collateral you're putting up. Pretty much the same process banks use, but they actually care about helping members instead of just profits. The whole thing gets reviewed once a year or whenever they need to make changes. Oh, and if you ever want to shake things up with their policies, you could always run for the board yourself. Most people don't realize they can actually do that.

Yeah, they're actually pretty solid with security. Your money's covered up to $250k through NCUA (same deal as FDIC but for credit unions). They use all the standard stuff - encryption, firewalls, secure logins. Plus they watch accounts round the clock for sketchy activity and will lock things down if something looks off. Here's what threw me off though - credit unions follow the exact same federal rules as major banks, which I honestly didn't know until recently. Some even throw in bonus stuff like identity theft protection. I'd just double-check what specific perks yours offers since they're all a bit different.

Your biggest edge is being the local, personal option - big banks can't touch that. Show off those better rates and lower fees, but honestly, the human touch is what really sells people. Social media's perfect for sharing member stories and community stuff you're doing. Get out there - sponsor local events, partner with businesses, volunteer at schools. That face-to-face connection still matters so much in banking. Oh, and don't forget your current members! They're your best salespeople if you keep them happy and actually remind them about referral perks.

So credit unions are really upping their game right now with digital stuff - mobile apps, AI chat features, online loan applications. They're still doing the whole community thing but also trying to attract younger members who want that cooperative vibe without clunky tech. Some are getting creative with fintech partnerships too, which is cool to see. My cousin just switched to one and loves it. They're also expanding who can join to compete with bigger banks. Short version: if you've been thinking about switching, this is probably the perfect time since they're actually modern now.

No Reviews