Fintech startup investor funding elevator pitch deck ppt template

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Fintech innovation around digital payments reduces costs and expand access for new clients to payment means. The high use of Fintech has resulted in a negligible effect on GDP and job creation. Advanced digital solutions that are flexible and secure are changing the way for startups. Here is a professionally designed pitch deck on Fintech Startup Investor Funding to offer digital services tailored to each customers needs. The template displays the pain points faced by customers and proposes solutions to entice the audience to resolve conflicts. Firms can check on why our product is better than others in the market and showcase technical advantages. The proposal guides you in presenting a complete view of the competitive landscape for investors. One can demonstrate the well-defined business models covering details about startup license and the Fintech model. The pitch deck portrays the activities the company will perform to grow its business. Businesses can exhibit ideas on product reviews with remarkable proof based on the simplicity and elegance of the product interface. Pitch investors for your company by explaining the yearly success timeline with posts of past experiences. Drop your requirement to us and talk to our expert for all your queries. Get access to the Fintech Startup Investor Pitch Deck now.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

Slide 1: This slide displays the title i.e. 'FinTech Startup Investor Funding Elevator Pitch Deck' and your Company Name.

Slide 2: This slide presents the table of contents for the pitch deck.

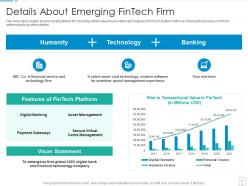

Slide 3: This slide caters details about emerging fintech firm including details about vision statement, features of FinTech platform addressing its growth potential.

Slide 4: This slide caters details about key facts associated to FinTech firm in terms of customers associated to it, average savings per company, average time to roll out etc.

Slide 5: This slide caters details about milestones achieved by FinTech firm over several years presented in timeline format.

Slide 6: This slide presents key challenges faced by prospects in terms of cost, time consuming process, no control over employees’ spending, outdated bank interface system, etc.

Slide 7: This slide caters details about unified solutions to address concerns faced by clients with overall expense reduction, streamline approvals, etc.

Slide 8: This slide caters details about services that are rendered by FinTech firm at global scale.

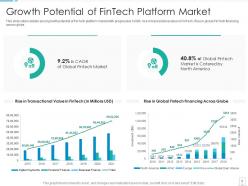

Slide 9: This slide caters details about growth potential of FinTech platform market with progressive CAGR, rise in transactional value, global FinTech financing across globe.

Slide 10: This slide caters details about market share of major FinTech platforms existing in market across globe.

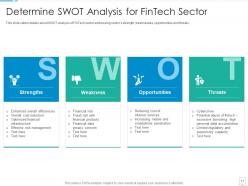

Slide 11: This slide caters details about SWOT analysis of FinTech sector addressing sector’s strength, weaknesses, opportunities and threats.

Slide 12: This slide caters details about competitive landscape of various competitors existing in FinTech platform market by comparing them on various parameters/ features.

Slide 13: This slide caters details about various metrics portraying FinTech platform progress in terms of rise in active users and rise in revenue.

Slide 14: This slide exhibits negative churn rate which determines that FinTech firm has been successful in retaining customers and ensuring them.

Slide 15: This slide caters details about value proposition by fintech platform by focusing on rendering rapid and effective solutions to customers.

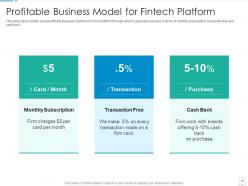

Slide 16: This slide presents profitable business model for FinTech platform through which it generate revenues in terms of monthly subscription, transaction fee and cash back.

Slide 17: This slide caters details about clients associated to FinTech platform in terms of major clients and client testimonials. .

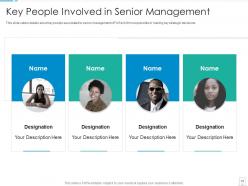

Slide 18: This slide caters details about key people associated to senior management of FinTech firm responsible in making key strategic decisions.

Slide 19: This slide caters details about board of members and advisors associated to FinTech platform.

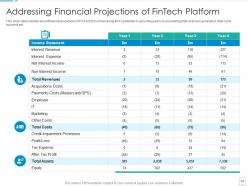

Slide 20: This slide displays financial projections of FinTech firm showcasing firm’s potential in upcoming years based on total revenues generated, total costs incurred, etc.

Slide 21: This slide caters details about future initiatives by FinTech platform that will focus on leveraging connections across potential stakeholders.

Slide 22: This slide showcases the contact details of the company.

Slide 23: This is the icons slide for the project.

Slide 24: This slide presents the title for additional slides.

Slide 25: This slide displays about the company, its client's value and target audience.

Slide 26: This slide displays the vision, mission and goals of the company.

Slide 27: This slide showcases the details of the team members.

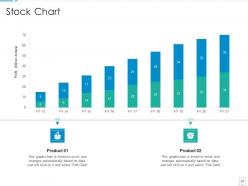

Slide 28: This slide presents the stock charts for products. The charts are linked to Excel.

Slide 29: This slide presents the line charts for products. The graphs are linked to Excel.

Slide 30: This slide displays the financial of the company.

Slide 31: This slide presents the comparison of the products.

Slide 32: This slide showcases the 30-60-90 days plan of the project.

Slide 33: This slide displays the magnifying glass projection of the company.

Slide 34: This slide displays the goals of the company.

Slide 35: This slide displays the posts for past experiences of the clients.

Slide 36: This is the thank you slide and contains contact details of the company like address, phone no., etc. "

Fintech startup investor funding elevator pitch deck ppt template with all 36 slides:

Use our Fintech Startup Investor Funding Elevator Pitch Deck Ppt Template to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Fintech startup investor funding elevator pitch

Dude, AI is literally everywhere in fintech right now - fraud detection, credit scoring, investment advice, you name it. Embedded finance is massive too. Like how Uber does that instant pay thing? That's non-financial companies just building banking right into their apps. BNPL is still exploding, though regulators are starting to crack down. Open banking APIs are making everything more competitive, which is cool for users. Honestly? If I were investing in this space, I'd look hard at RegTech companies. Everyone's drowning in compliance stuff and they'll pay big money to fix those headaches.

Honestly, regulation is kind of a mixed bag for fintech right now. Yeah, compliance costs are brutal and you'll definitely launch slower with all the data privacy and crypto rules. But investors actually like the clearer guidelines - makes them way less nervous about cutting bigger checks. The smart startups I've seen bake compliance in from the start instead of scrambling later (which is expensive as hell). My take? Don't even think about scaling without nailing your regulatory game first. It's boring but it'll save you tons of headaches down the road.

Dude, blockchain could seriously shake up banking. Cross-border payments would be instant instead of taking forever like they do now. Everything gets recorded on this ledger that's basically impossible to hack or mess with. Smart contracts handle stuff like loan approvals automatically - no more waiting around for some banker to get back from lunch, you know? It's also huge for people who can't get regular bank accounts. Oh, and if you're looking at fintech stuff, I'd probably start with payments or lending since that's where most of the action is happening right now.

Dude, AI is totally changing fintech right now. Chatbots actually get what you're asking instead of giving you random responses. Your apps learn how you spend and suggest better ways to save - some of this stuff is honestly creepy good. Real-time fraud detection catches sketchy transactions before they hit your account. Oh, and all the tedious paperwork gets automated, so when you do need human help, they're not buried in boring tasks. I'd definitely look for apps with AI features - you'll get way better financial insights and save tons of time.

So P2P lending basically lets regular people fund your loan instead of going through a bank. You'll often get better rates that way, plus faster approval - especially if your credit is decent but not amazing. LendingClub and Prosper are the big ones. Way less paperwork than banks, though they still check your credit obviously. Only thing is these companies aren't as stable as banks, so they could change their terms or whatever. I'd definitely shop around and compare their rates with traditional lenders too. Honestly, the difference might shock you. Worth checking out if you need cash.

Dude, fintech security is no joke - you're dealing with data breaches, payment fraud, identity theft, all that fun stuff. People are basically handing you their financial lives, so yeah, pressure's on. Multi-factor auth is your best friend here, plus you need solid encryption and fraud detection running 24/7. Don't sleep on compliance either - PCI DSS and GDPR will bite you if you're not careful. Honestly, I'd stack multiple security layers rather than betting everything on one system. Oh, and definitely get a security audit done first to see where you actually stand right now.

Dude, COVID basically fast-tracked fintech by like 5 years overnight. My parents who still write checks suddenly figured out Venmo - that's how crazy it got. Everyone downloaded banking apps since branches were closed, and contactless payments became the norm real quick. Small businesses had to scramble for digital solutions when banks were totally overwhelmed. Honestly, it forced people's hands in the best way possible. Now there's this huge wave of new users who expect everything to work smoothly. If you're jumping into fintech, just remember those people got spoiled by crisis-mode user experience - they won't settle for clunky apps anymore.

So fintech companies are basically stalking your digital life to make money decisions. They're analyzing your transaction history, social posts, even where you shop to instantly approve loans or catch fraud. Wild stuff, right? The same data helps them customize products just for you and figure out pricing. Oh, and they can predict your behavior from your online habits - kind of creepy but also impressive. If you're diving into this field, start with quality data collection. Your algorithms won't work if you're feeding them junk data first.

Honestly, the consent thing is huge - people just don't get what data you're actually grabbing or why. And let's be real, when someone needs your app to manage their finances, saying "no" to data sharing isn't really an option, right? That's not genuine consent. You're also holding incredibly sensitive stuff that could ruin lives if it gets breached or misused. The whole challenge is innovating without screwing over users (easier said than done). I'd start with privacy audits and - this sounds boring but matters - making your privacy policy actually readable instead of legal gibberish.

So fintech just cuts through all the BS that banks put up - no branches, no crazy minimum balances, none of that paperwork nightmare. People can literally do everything from their phone now, which is amazing for anyone who doesn't live near a bank or can't afford those ridiculous fees. Microloans and digital wallets make things so much cheaper too. The whole approval thing is way faster since they're not stuck in 1995 like traditional banks lol. Oh and if you're building something in this space, definitely make sure it works on basic phones - that's honestly where you'll help the most people.

Look, crypto payments are pretty sweet for international stuff - way faster and cheaper than banks. No chargebacks either, which is huge. Your customers get privacy too. But dude, the price swings are insane. One day you're up, next day you're down 20%. The regulations are still a mess everywhere, and honestly? Half your customers probably don't even know how to use it yet. Oh, and the environmental thing might bite you if you care about that image. I'd maybe try it with like 10% of transactions first, see how it goes before diving in headfirst.

Dude, robo-advisors are pretty solid if you're just getting started. Most let you begin with like $500 instead of those crazy $100k minimums traditional advisors want. They'll automatically spread your money across different investments, rebalance everything, and do that tax-loss harvesting thing - basically runs itself. Fees are way cheaper too, maybe 0.25% vs the 1-2% human advisors charge. Yeah, you don't get to actually talk to someone, but honestly? For basic investing that's probably fine. I'd check out Betterment or Wealthfront if you want something simple that just works.

Honestly, AI and machine learning are everywhere now - fraud detection, personalized banking, automated trading. Quantum computing might completely change encryption and risk stuff, but that's still years away probably. Blockchain's finally getting real use cases beyond just crypto - cross-border payments and smart contracts actually work. DeFi platforms are interesting too, plus embedded finance where you can get loans through like, your Uber app or whatever. Biometric auth is making passwords feel super outdated. But here's the thing - don't try tracking all this at once. Pick one or two areas you actually find interesting and go deep on those instead.

So banks and fintechs can team up in a few ways - API integrations, white-label stuff, joint ventures. The whole idea is banks bring regulatory know-how and trust, while fintechs bring speed and innovation. Works great when banks license fintech payment tech or when fintechs lean on banking infrastructure for compliance. Makes total sense since banks are slow to adapt but fintechs need that regulatory backbone (and honestly, the capital too). Best partnerships happen when each side sticks to what they're actually good at instead of trying to do everything. I'd look for spots where partnerships fill obvious holes in what you're currently doing.

Honestly, payment processing and digital banking are killing it right now. Stripe's basically owning payments, while neobanks like Chime are crushing traditional banks on user experience. Alternative lenders are pretty smart too - they're using AI to approve loans way faster. Here's the thing though: B2B fintech is where you actually make bank since businesses pay so much more than regular consumers. Subscription models work best because the revenue's predictable. My advice? Don't try building some massive "do everything" app. Pick one specific problem and nail it perfectly. That's honestly how you win in this space.

-

Very unique and reliable designs.

-

Awesomely designed templates, Easy to understand.

-

Excellent products for quick understanding.