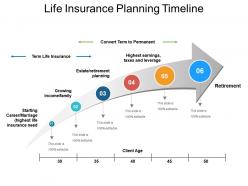

Life insurance planning timeline

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Increase their chances of achieving goals with our Life Insurance Planning Timeline. It enables better grooming.

People who downloaded this PowerPoint presentation also viewed the following :

Life insurance planning timeline with all 5 slides:

Depend on our Life Insurance Planning Timeline to make the cut. They will help you plan your play.

FAQs for Life

Look, the biggest thing is replacing your income if something happens to you - keeps your family from scrambling financially. It'll cover the mortgage, kids' college, all that stuff. Some policies build cash value you can borrow against later, but honestly? There are way better investments out there. The estate planning angle is solid though - pays those nasty estate taxes so your family doesn't have to sell everything. Really though, it's about peace of mind. Figure out what your family would actually need (debts, expenses, etc.) then start shopping for term life insurance. Way cheaper than whole life and gets the job done.

So here's the deal - term life is cheap and covers you temporarily, like while you've got a mortgage or little kids running around. Perfect for most people starting out. Whole life costs a ton more but you can actually borrow against it later, which is nice for estate planning stuff. Honestly, I'd probably go term first since it's way more affordable and covers the major stuff you're worried about. My cousin went straight to whole life and kinda regrets how much she's paying monthly. Just think about whether you need this forever or just for now - that'll basically tell you which way to go.

Honestly, forget that "10 times your salary" thing - it's way too simple. Start by adding up what'd actually hit your family: mortgage balance, credit cards, any loans. Then think about ongoing stuff like the kids' college, daily expenses, maybe helping your spouse retire someday. What would they really need to keep living the same way without your paycheck coming in? I'd mess around with one of those needs calculator things online first (they're actually pretty helpful), then maybe chat with an agent who can look at your specific mess of finances and help you nail down the real number.

So life insurance is actually a solid move for passing money to your kids without the tax headache. The death benefit goes straight to them tax-free, which beats most other inheritance stuff. You can use it to cover estate taxes too - saves your family from having to sell the house or whatever to pay Uncle Sam. There's this thing called an irrevocable trust that removes the whole policy from your estate (sounds complicated but it's not). Honestly, the tax benefits are pretty impressive. Definitely worth chatting with an estate attorney about how it fits your situation.

So basically, insurance companies look at your age and health to figure out how much to charge you. Younger + healthier = cheaper rates. Pretty straightforward math on their end. Once you hit certain ages or develop health problems, they'll jack up the price since you're riskier to insure. Honestly, this is why I always tell people to get coverage early, even if you think you don't need much right now. My cousin waited until his 40s and his premiums were like double what mine are. Lock in those rates while you can - future you will thank you for it.

Every 3-5 years is the general rule, but honestly? Life events matter way more. Marriage, divorce, kids, new house, job switch - that's when you really need to look at your coverage. I learned this the hard way when I realized I was still listed as single on mine for like two years after getting married. Your needs change faster than you think. Short sentences work here. Also worth checking if your health's improved since you first got the policy - you might snag better rates. Just set a reminder on your phone for your anniversary date and don't ignore it.

Dude, don't fall for that myth about life insurance being just for old folks or the main breadwinner. Young and healthy means way cheaper rates. Stay-at-home parents need it too - have you seen what daycare costs these days? Your work policy probably sucks and vanishes when you quit anyway. Here's the thing though - it's not nearly as pricey as people think. A healthy 30-year-old can get decent term coverage for like $20-30 a month. Just shop around because some companies are weirdly expensive compared to others for the exact same thing.

Hey! So permanent life insurance like whole life has this cash value thing that builds up over time. Part of your premium covers the death benefit, but the rest goes into what's basically a savings account that grows tax-deferred. You can actually borrow against it or pull money out while you're alive, which is pretty neat. Honestly though, it's way more expensive than term life. I'd definitely crunch the numbers against just buying term and investing the difference - sometimes that comes out ahead. Really depends on your tax situation and what other investment options you've got available.

Hey! So here's the deal - life insurance payouts are usually tax-free for your beneficiaries. Like, they won't owe anything on the main death benefit amount, which is honestly pretty great. The only catch is if there's interest involved (say the insurance company sits on the money for a while), then yeah, they'd pay taxes on that interest part. Oh, and there are some weird exceptions with employer policies or if someone sold their policy beforehand, but that stuff's rare. Your beneficiaries should definitely know they're in the clear on the actual payout though.

So riders are basically add-ons for your life insurance - they let you customize beyond just the basic death benefit. You can get disability income riders if you can't work, or accelerated death benefits to access money early if you're terminally ill. There's also accidental death coverage, long-term care stuff, child riders for your kids. Honestly, some of the newer ones are pretty clever. But don't just buy everything they offer you - that's how they get you spending way more than needed. Figure out what coverage gaps you actually have first, then pick riders that make sense for your situation.

Look, I'd say convert when you realize you'll need coverage forever, not just temporarily. Maybe you've got estate planning stuff now, or you want to guarantee leaving something behind. The timing's usually best while you're still healthy but aging - nobody likes thinking about this crap, but that's reality. Since you're already covered, you skip the medical exams and all that hassle. Just heads up though - your premiums are gonna shoot up big time. My cousin did this and was shocked at the jump. Make sure you can actually afford it long-term before you commit.

Definitely shop around with at least 3-5 companies - the rate differences are insane for identical coverage. An independent agent can do the legwork if you're lazy about it. Apply when you're healthy and actually prepare for that medical exam. Don't roll in hungover like my cousin did lol. Age matters too, so if you're thinking about it, just do it. Rates go up every year you wait. Get everything in writing and compare the actual policy details, not just monthly payments. Oh and don't just go with the cheapest - read the fine print.

Honestly, just get everything together upfront - all your forms, medical records, financial docs, the whole mess. Don't piece it together later. Book that medical exam right away and don't reschedule unless you're literally dying (they get annoyed). Be completely honest about your health stuff because they're gonna find out anyway through tests and records. When they ask for more info later, jump on it immediately. Most people take forever responding and that's what slows everything down. Quick responses = quicker approval.

First thing - check their A.M. Best ratings (A- or better). These companies need to actually pay up when you file a claim. Compare quotes from 3-4 different places and read real customer reviews online. Your state insurance department tracks complaint ratios too, which is super helpful. Those door-to-door sales people? Hard pass - they're usually pushing garbage policies. Stick with the big established names that have been doing this forever. I mean, there's a reason State Farm and Allstate aren't going anywhere. Make sure whoever you pick is licensed in your state before signing anything.

Look, if something happens to you and you don't have life insurance, your family's basically screwed financially. Your income disappears but the mortgage, kids' college fund, groceries - all that stays the same. I've seen friends whose spouse had to sell their house and drain retirement accounts just to survive. Plus getting coverage when you're young is way cheaper than waiting until you're older (or god forbid, have health issues). I know it's depressing to think about, but honestly? It's one of those adulting things you just gotta handle.

-

Use of different colors is good. It's simple and attractive.

-

Appreciate the research and its presentable format.