Digital Transformation in Banking Industry Training ppt

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

The PPT training deck provides a comprehensive overview of digital transformation in the banking industry. It includes the benefits of digital banking for customers, such as personalized service and real-time remote access, as well as advantages of digital transformation to banks, such as staying in sync with ever-evolving consumer needs. The PowerPoint module also covers factors that drive digital transformation in the banking industry along with the implementation challenges, such as the limited acceptability of an entirely digitized bank and internal barriers. It also includes innovations in the digital banking industry, such as advanced self-service capabilities, instant payments, and chatbots. Further, the deck covers the use case of big data and blockchain technology in banks and the advantages of neo-banking. It includes PPT slides on peer-to-peer P2P lending, DeFi Decentralized Finance, and investment banking. It also contains case studies and discussion questions to make the training session interactive. Digital Transformation PPT slides on about us, vision, mission, goal, 30-60-90 days plan, timeline, roadmap, training completion certificate, and energizer activities.

People who downloaded this PowerPoint presentation also viewed the following :

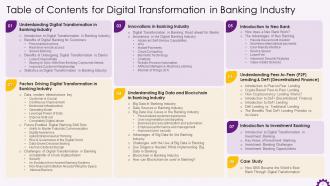

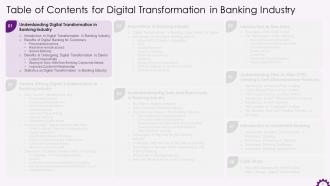

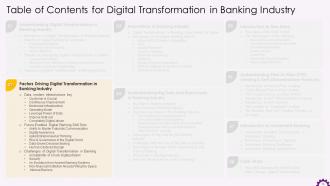

Content of this Powerpoint Presentation

With the advent and continuing development of technologies, everything around us is changing, and the banking sector is no exception. Thus, inevitably, digital transformation impacted the banking industry more than other spheres, increasing the value of training and communication.

Understanding the necessity of clearing the ground for your bank's successful future in and through digital transformation, SlideTeam has excellent presentation slides that meet your challenges. Our Digital Transformation in Banking Industry Training PowerPoint has been designed to facilitate an understanding of the essential principles and objectives of the new reality of the banking industry. You will get a complete toolbox intended to provide banking professionals with the information, tactics, and tools they need to succeed in the digital world.

By the end of the presentation, you will come across digital transformation concepts as well as captivating images that engage and enlighten, allow banks to embrace change, grasp opportunities, and chart a road toward a more digitally focused future.

Do not see digital transformation as a threat. See it as a new opportunity to change and take it with SlideTeam's Digital Transformation in Banking Industry Training PPT to back you up.

Stay in the loop with our captivating blog on Digital Transformation PowerPoint presentation for a fantastic journey.

Template 1 - Introduction to Digital Transformation in Banking Industry

![]()

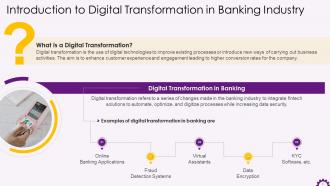

The slide functions as the introduction to digital transformation in the banking industry. Firstly, it introduces the concept and characteristics of digital transformation before specifying the most prominent tools related to it in the banking industry. Through a visual representation and concise descriptors, it demonstrates how virtual assistants, fraud systems, encryption of data, know-your-customer (KYC) software, and online banking are used within the sector to enhance its operation. It could be applied to a series of training sessions for banking professionals, which provides an essential introduction to the topic.

Template 2 - Benefits of Digital Banking For Customers - Personalized Service

![]()

On this slide, you can learn more about the contribution of digital banking to transformation, which is associated with its ability to provide personalized services to customers. The slide tells that personalized banking is about offering products that correspond to where customers are in their relationship with the bank. Overall, personalized banking is about offering financial solutions that meet the demand of customers, large or small, through extensive data analysis. It is beneficial for educational purposes and could be used within the banking industry to educate staff on the importance of the implementation of personalized service tools.

Template 3 - Benefits of Digital Banking For Customers - Real - Real-Time Remote Access

![]()

This slide elaborates upon real-time remote access as one of the most significant benefits that digital banking has to offer to its customers. It explains that digital banking is all about autonomy because people can access their accounts at any time and from any distance, making transactions in real time. It includes critical skills that would be training the banking staff responsible for customer service, digital transformation, and product development about the necessity of providing real-time access to customers to meet their expectations and satisfy their needs.

Template 4 - Benefits of Digital Banking For Customers - Secure Banking

![]()

The slide focuses on promoting the idea that secure banking is the foundation of digital banking from a customer's perspective. It provides an example of how banking websites and mobile applications utilize robust security features to protect customers' sensitive personal information. In addition, it explains the ways in which customers can become proactive in managing their secured access to online banking by learning to recognize phishing emails, creating safe passwords, and establishing account alerts. While referring to the training for employees working in the banking industry and connected with customer service and digital transformation, the slide ensures that they understand that securing customers' sensitive information is critical for fostering their confidence.

Template 5 - Benefits of Adopting Digital Banking to Banks - Lower Dropout Rate

![]()

This slide provides a list of benefits related to the implementation of digital transformation by banks and highlights a lower dropout rate. The slide shows how the application of this technology will improve the loyalty level of customers and explains how it helps enhance retention. Furthermore, it gives detailed information on the necessity of following consumer trends and the goals of using digital tools to improve customer relationships. The slide is designed to be presented during banking industry training courses to the top managerial staff. This cadre handles strategic implementation of new ideas concerning engagement with customers.

Browse through our blog on Building Digital Strategy Roadmap for digital transformation for engaging reads.

Template 6 - Benefits of Adopting Digital Transformation to Banks - Staying in Sync With Ever-Evolving Consumer Needs

![]()

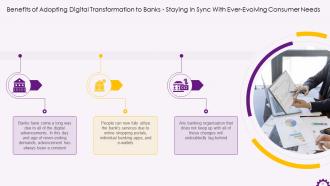

This slide focuses on the benefit of digital transformation for banks in terms of keeping up with customer demands. It presents a contrasting image of the past and the present to highlight the changes. Digital banking has significantly changed the way businesses operate. It has transformed customers' ability to truly engage in its benefits through shopping online and using banking applications and e-wallets. By integrating with digitization, banks can meet the ever-changing demands of their customers and, therefore, increase customer satisfaction and loyalty. This slide is essential to the banking industry training as it informs the relevant stakeholders about the necessity of being digitally transformed. It also works to ensure that necessary software integration is done to allow them to keep up with customer demands.

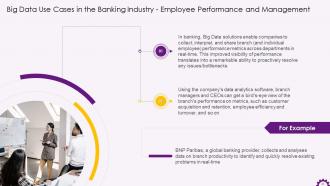

Template 7 - Benefits to Banks By Adopting Digital Transformation - Improved Customer Relationship

![]()

This slide highlights the primary benefit of digital transformation in banking, which is improved relations with customers. The problem that the slide addresses is that it is challenging to maintain good communication with customers. Big data-centered solutions in the evolving digital environment enable the carefully structured collection of information to track customer preference. As such, the technologies and tools allow the creation of customized services and approaches for working with the customers themselves. Customer-centered technology is the primary tool that will significantly help the banking sector enhance customer satisfaction in the long run.

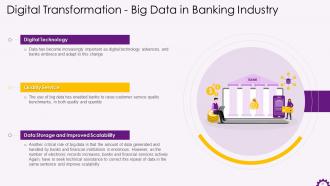

Template 8 - Digital Transformation in Banking Industry - Key Statistics

![]()

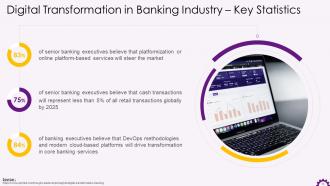

This slide provides some robust statistics that show how digitalization changes the banking sector. It includes comments made by business people who explain that platformization and DevOps methodologies would alter the banking industry. More cashless transactions and different practices will be applied, which was impossible earlier. It can be used in training sessions for bank employees since they can get such statistics and understand digital transformation.

Template 9 - Future Enabled Skills in Digital Banking-Ability to Master Futuristic Communication

![]()

This slide taps into the urgent need for customer engagement at a time when physical bank branches are diminishing and traffic to mobile banking services is reaching unprecedented heights. Arguably, mobile banking is becoming the cornerstone of the banking business. Therefore, innovative banks are leveraging digital channels to not only precisely map the customer journey but also provide tailored solutions. Finally, future-ready banks take advantage of modern multifactor authentication methods to ensure the highest level of security. By mastering futuristic communication skills, banks can win the digital transformation race and remain in close contact with the customer.

Template 10 - Future Enabled Skills in Digital Banking-Digital Awareness

![]()

This slide accentuates the importance of digital awareness as a critical skill in digital banking. It explains that digital platforms are increasingly the leading avenue for customer engagement across the globe. Utilizing these avenues helps banks meet customer needs and subsequently increases brand loyalty among customers. The banking profession is experiencing rapid technological change, meaning bank professionals must stay updated on new tools, some of which stand to cost the banks of tomorrow. Having digital awareness will help people anticipate these new tools and understand their business implications, whether currently or in the future.

Taking the Banking Sector to A Whole New Level

Recognizing the need for banks to change or risk obsolescence, these slides are designed to handle the difficulties of the digital age. Moreover, slides help you look at digital transformation in the banking industry from unique vantage points and equip you with a deeper understanding of the cases. Moreover, slides are easy to edit, 100% content-friendly, and easy to download in PNG and jpg formats.

PS Don't miss out on our enriching blog on Digital Transformation Digital Organization Analytics for more knowledge.

Digital Transformation in Banking Industry Training ppt with all 110 slides:

Use our Digital Transformation in Banking Industry Training ppt to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Digital Transformation in Banking

Honestly, it's all about keeping up with what people expect now. Everyone's used to Amazon and Apple making everything stupid easy, so they want their banking to work the same way - mobile apps that actually work, instant everything, stuff that feels made for them. Fintech companies are crushing it because they get this better than old banks do. The money side matters too though - digital stuff costs way less to run than having branches everywhere. Regulators want better data systems anyway. My advice? Figure out what YOUR customers actually need digitally before you start buying whatever some sales guy is pitching you.

Honestly, AI can totally transform how banks handle customers. Chatbots are a game-changer for 24/7 support - no more waiting on hold forever. Fraud detection happens in real-time now, which is awesome. Voice assistants let people check balances just by talking, though I still prefer the app personally. The personalization stuff is where it gets really interesting - AI analyzes spending habits to suggest relevant products or catch weird transactions before customers even notice. My advice? Figure out what's currently driving your customers crazy, then find the AI tools that fix those specific problems first.

Honestly, banks are basically running on data now instead of just winging it like they used to. They catch fraud as it's happening, figure out what products you'd actually want, and assess credit risk way better than before. Pretty crazy how they can predict your spending habits, right? Also helps them staff branches properly and price loans. Oh and here's a tip - when you're talking to your bank, ask what data they're using for their recommendations. They'll step up their game when they realize you get how this stuff works.

Dude, fintech is seriously shaking things up for banks right now. Like, customers expect instant transfers and slick apps - none of that 3-5 business day nonsense anymore. Banks are panicking because honestly? Their old systems are trash compared to what these startups offer. So now they're either partnering with fintechs or desperately trying to build their own modern platforms. The whole industry's being forced to catch up or get left behind. If you're in banking, you'd be smart to watch what the hot fintech companies are doing and steal their best ideas before someone else does.

Honestly, the biggest pain is how your attack surface just explodes with all these new digital entry points. Legacy systems are a nightmare when you're trying to mesh old tech with new stuff - there's always some weird vulnerability hiding. Data breaches cost way more now too, which is terrifying. Plus you've got compliance headaches across different regions, identity management that's gotten crazy complex, and customers who want everything to work perfectly AND be totally secure. Oh, and here's the thing - build security in from the start. Don't try to patch it on later because that never works out well.

Honestly, don't wait until the end to think about compliance - that's a nightmare waiting to happen. Map out which regulations hit your new digital stuff first. Your legal team might slow things down sometimes, but they're actually saving you from major headaches later. Build solid data governance right into everything, especially anything touching customer info. I learned this the hard way on a project once - privacy requirements are no joke. Treat compliance like any other feature you'd build. Automate the monitoring parts where you can so you catch problems before they blow up.

Mobile banking apps work best when they actually solve problems people have. Personalized spending alerts and financial insights keep users coming back - way better than generic notifications that just annoy everyone. The real winners focus on seamless transfers, bill pay, and budgeting tools that don't suck. Push notifications are great but honestly, most apps overdo it and people just turn them off. I'd say pick a few features that genuinely help with daily banking headaches instead of building some kitchen-sink app. Quick access to what you need most - that's what gets people hooked.

Honestly, digital transformation is a game-changer for bank efficiency. Automation handles all the tedious stuff - loan processing, onboarding new customers, back-office tasks. No more manual errors eating up everyone's time. Your team can actually focus on meaningful work instead of paperwork hell. Real-time analytics show you exactly where things are getting stuck too. My advice? Look at whatever processes currently make you want to pull your hair out - start there. Those are usually your biggest opportunities for improvement. The AI tools today are actually pretty solid at handling repetitive work.

Your customers are literally comparing you to Netflix and Uber now, not just other banks. They want accounts opened in minutes, real-time alerts for everything, and chatbots that don't suck. The whole "come into a branch" thing? Dead. People expect banking to feel like every other app - instant and actually intuitive. Honestly, they're even wanting proactive stuff now, like heads up before overdrafts hit or personalized money tips. It's kinda wild how fast expectations shift. I'd start by testing your mobile app against whatever non-banking apps your customers obsess over.

Honestly, focus on three things first: cloud infrastructure, APIs, and data analytics. Cloud gives you the scalability you need without breaking the bank long-term. APIs are huge for integrating with fintech partners - you can't do much without them. Analytics helps you figure out customer patterns and spot sketchy behavior. AI/ML is pretty much expected now, especially for fraud stuff. Mobile-first is obvious since everyone's glued to their phones. If you haven't moved to cloud yet, do that first. It's annoying upfront but unlocks everything else.

Build security into everything from the start - don't just slap it on later. Honestly, risk teams working alongside developers is huge. Start with small pilots so you're not risking everything while you figure things out. Nobody wants to end up as tomorrow's banking disaster story, but you can't let fintechs steal all your customers either. Set your risk limits upfront, get some automated monitoring going, and create feedback loops. That way you can move fast without breaking compliance rules. Cross-functional teams are really where the magic happens though.

Honestly, I'd focus on customer adoption rates and digital transaction volumes first - those tell the real story. Cost-per-transaction reduction is huge too, plus customer satisfaction scores for your digital stuff. Revenue from digital products will make the executives happy, which matters more than we'd like to admit. System uptime and app store ratings are pretty critical since nobody uses broken apps. Oh, and track how fast you're shipping new features - that one's easy to forget but stakeholders love seeing progress. Pick maybe 3-5 metrics max though, don't go crazy trying to measure everything.

So blockchain is basically this shared ledger that nobody can mess with - everyone trusts the same data. Cross-border payments that used to take forever now happen in hours. Trade finance speeds up like crazy too. All that paperwork just vanishes, which honestly feels too good to be true but it works. The best part? You cut out all these middleman steps that eat up time and money. KYC processes get way smoother. If you're thinking about trying it, don't go big right away - start with something internal like audit trails first.

Honestly, banks are terrible at this but here's what actually works. First off, people won't try new stuff if they're scared of getting fired for mistakes - psychological safety matters. Give teams dedicated time for experiments (Google does 20% time). Mix your tech people with business folks, they need to talk more. Celebrate the failures that teach you something, not just wins. Your executives have to visibly use the digital tools too or everyone sees through it. Hackathons are good, plus rotate people through fintech partnerships. Find your internal digital nerds and let them spread the excitement naturally.

Banks are going nuts with encryption layers and giving customers way more control - like choosing exactly what data gets shared. Honestly, the regulatory stuff is probably doing the heavy lifting here. GDPR and those banking rules have everyone scrambling. Most are throwing money at zero-trust security models too. Third-party audits happen constantly now. The real shift though? Transparency initiatives. Customers don't just want "trust us, it's secure" anymore - they actually want to understand what's happening with their info. Makes sense after all the data breaches we've seen.

-

Out of the box and creative design.

-

Great experience, I would definitely use your services further.