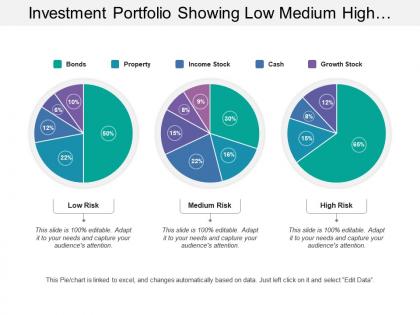

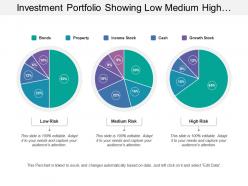

Investment portfolio showing low medium high risk with bonds and growth stocks

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Expose the flaws in an intolerant approach with our Investment Portfolio Showing Low Medium High Risk With Bonds And Growth Stocks. Be able to challenge the bigots.

People who downloaded this PowerPoint presentation also viewed the following :

Investment portfolio showing low medium high risk with bonds and growth stocks with all 6 slides:

Our Investment Portfolio Showing Low Medium High Risk With Bonds And Growth Stocks are a gas. They create a buzz of excitement.

FAQs for Investment portfolio showing low medium high risk with bonds

Honestly, you'll want to spread your money across different types of investments - don't put everything in tech stocks or whatever's trendy. Watch how your investments move together too, because if they're all tanking at once, that's a problem. Some sectors are just naturally more volatile (looking at you, crypto). Your timeline makes a huge difference though - longer investing periods mean you can weather the crazy ups and downs. Interest rates and economic stuff will definitely impact your returns. Oh, and rebalance periodically when things drift too far from what you originally planned. Just don't obsess over it daily.

Basically, don't put everything into one stock or sector - that's how people get burned. Mix it up with stocks, bonds, maybe some international stuff. The whole point is that when tech crashes (and it will), your other investments might actually go up or at least stay steady. It's like not putting your entire paycheck into crypto, you know? Within stocks, grab different industries so you're covered. Honestly, I learned this the hard way during the 2020 mess. You want assets that don't all tank together on the same day.

So correlation shows how much your investments move together - super important for actual diversification. Tech stocks? They usually crash as a team, which sucks if that's all you own. You want some stuff that moves differently when the market freaks out. Negative correlation is your friend here - smooths out those crazy swings. I learned this the hard way in 2020 when everything tanked together despite being "diversified." Check those correlation charts once in a while, especially when markets get weird. Relationships between assets shift more than you'd think.

Honestly, just think about three things: money, time, and your stress tolerance. How much can you actually lose without freaking out about rent or your kid's college fund? If you've got like 20+ years before you need the money, you can ride out more ups and downs than someone who's retiring soon. The hardest part though? Being real about how you'll handle watching your account drop 20%. Because trust me, it happens. Maybe think about other times money stress hit you - did you panic or stay cool? I'd say start small and conservative, then get bolder as you learn what you can stomach.

Standard deviation and beta are the big ones - they show volatility and how your stuff moves with the market. VaR tells you potential losses, which is honestly pretty crucial. Sharpe ratio's my favorite though because it shows if you're actually getting decent returns for the risk. Oh, and maximum drawdown - basically your worst nightmare scenario. I feel like people sleep on that one but it's super telling. Those five will give you a solid read on what's actually dangerous in your portfolio. Start there and you'll be way ahead of most people.

Volatility is just how much your investments bounce around - up one day, down the next. More volatility usually means higher potential returns, but honestly, it can be stressful to watch. You want to mix risky stuff like growth stocks with boring reliable things like bonds. Your age matters a ton here. Twenty-something? You can ride out the crazy swings for better long-term gains. But if you're like 10 years from retiring, probably time to chill with safer investments. Really comes down to whether you can handle watching your account balance do backflips without panicking.

Diversification is your best friend here - spread stuff across stocks, bonds, real estate, different sectors. Don't put everything in one place, obviously. Figure out your target percentages based on how much risk you can stomach. Younger people can usually handle more stock volatility since they have time to recover. Rebalancing is huge too - sell the winners, buy the losers to keep your allocation on track. I know it sounds backwards but it works. Oh and honestly? Start by figuring out if market swings will keep you up at night, then build from there.

Looking at historical data gives you patterns to work with - you can see how different assets performed during crashes, recessions, boom periods. It's like having a backward-looking crystal ball, which honestly beats flying blind. Calculate things like standard deviation and correlation to see how your investments might move together. Past performance doesn't predict the future though (I know, boring disclaimer). Use historical data as your starting point but definitely stress-test against scenarios that haven't happened yet. The math stuff can get tedious but it's worth doing.

So basically you're putting your portfolio through hell to see what breaks. Run it through scenarios like 2008 or the COVID mess - see which investments get destroyed and how badly your returns tank. It's morbid but you'd rather find out now than during an actual crash, right? Test different disasters: interest rates going nuts, whole sectors imploding, currency chaos. I usually start simple then make it more complicated (though honestly sometimes I get lazy with this part). Once you spot the weak links, you can rebalance or hedge before things go sideways.

So there's two types of risk you gotta worry about. Systematic risk hits everything at once - market crashes, recessions, Fed raising rates, that kind of mess. You can't really escape it. Unsystematic risk is different though. That's when one company or industry screws up, like if Tesla's CEO goes off the rails again (which honestly wouldn't shock me). The good news? You can actually fix unsystematic risk by spreading your money around different stocks and sectors. Systematic risk just comes with the territory of investing.

Yeah, so external stuff can really mess with your portfolio because it hits everything at once. Recession hits? Suddenly your "diversified" investments all tank together - super annoying. Interest rates, inflation, currency swings - they don't care about your careful asset allocation. Here's the kicker: when markets get stressed, correlations between different assets actually go up, which is basically the worst timing ever. Your strategy that worked fine during chill times might completely fail you. I'd say check macro trends regularly and maybe run some stress tests on your holdings.

Honestly depends on your budget. Bloomberg Terminal and FactSet are amazing but cost a fortune - only worth it if your company's paying. Morningstar Direct is decent for most portfolio stuff without breaking the bank. If you can code at all, definitely check out Python libraries like PyPortfolioOpt and QuantLib. They're surprisingly powerful and I've been using them way more lately. Excel works in a pinch with some Monte Carlo add-ins, though it gets messy quick. My advice? Start with whatever you already have access to first. See if it actually handles your risk modeling needs before spending serious money on the fancy tools.

I'd check quarterly if you're really hands-on with investing. Once a year minimum though. Big life stuff changes everything - new job, marriage, house purchase, getting closer to retirement. Your risk tolerance shifts way more than people realize. Market crashes or booms mess with your actual allocation too, even when your goals stay the same. Honestly, most people wait until something bad happens instead of staying ahead of it. Set a phone reminder every few months for a quick gut check. Does your portfolio still feel right for where you're at? Takes like 10 minutes but saves headaches later.

Market conditions totally change how you should handle risk - what crushed it during bull runs can absolutely wreck you when things flip. Your tech-heavy portfolio probably felt brilliant in 2020, then... yeah, 2022 happened. Interest rates mess with everything, inflation shifts the game, and suddenly all your correlation bets are wrong. You've gotta stay flexible here. Test different scenarios regularly, not just when stuff starts tanking. Honestly, I learned this the hard way - don't wait until you're already bleeding to adjust your approach.

Dude, regulatory changes totally flip risk assessment on its head. New compliance rules pop up, capital ratios shift, they force different measurement methods - it's chaos. Basel III was a perfect example - banks had to redo their entire risk models overnight. You've gotta update frameworks, run new stress tests, maybe even restructure whole portfolios to hit these fresh thresholds. Honestly, the worst part is playing catch-up after rules drop. Try setting up alerts for proposed changes and build some wiggle room into your models. Makes adapting way less painful when the next curveball hits.

-

Use of icon with content is very relateable, informative and appealing.

-

Excellent design and quick turnaround.