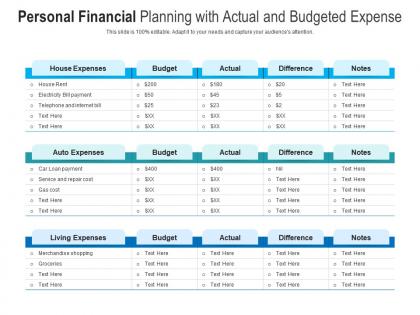

Personal financial planning with actual and budgeted expense

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Our Personal Financial Planning With Actual And Budgeted Expense are topically designed to provide an attractive backdrop to any subject. Use them to look like a presentation pro.

People who downloaded this PowerPoint presentation also viewed the following :

Personal financial planning with actual and budgeted expense with all 2 slides:

Use our Personal Financial Planning With Actual And Budgeted Expense to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Personal financial planning with actual

So first thing - track your spending for like a month because honestly, most of us have no clue where our money goes. Build up that emergency fund (3-6 months expenses) before doing anything else. Once you've got that cushion, go hard on paying off credit cards and high-interest debt. Then you can start investing - max out your 401k match if your job has one, open an IRA, stick with boring index funds. Oh and get some basic insurance and write a will (I know, super fun stuff). Just pick one thing and start there though - you don't need to do everything at once.

First thing - figure out your actual net worth. List everything you own (savings, house value, investments, whatever) then subtract all your debts. Credit cards, student loans, mortgage, the whole mess. That gives you your starting point. Also track your spending for like a month - I know, super fun right? But write down what comes in vs what goes out. Trust me, you can't fix what you can't see. Once you've got those numbers down, problem spots become pretty obvious. Same with opportunities you might've missed.

Honestly, you can't really get your finances together without knowing where your money's going. I used to think budgeting was this huge complicated thing, but it's literally just writing down what comes in vs what goes out. Track everything for like a month - you'll probably be shocked at how much you spend on random stuff. Once you see the patterns, you can figure out how much to actually save or throw at debt. It stops you from buying dumb things too (guilty as charged). Just start simple and tweak it as you go.

Look, having different timeframes for your goals just makes everything way clearer. Emergency fund first - that's your short-term sanity saver. Then medium stuff like house down payments keeps you focused without blowing up your other plans. Retirement and college funds? Those are the big picture goals that should guide your major money moves. I swear, it's like finally having GPS instead of wandering around Target with a credit card. Oh, and definitely write down one goal for each timeframe with actual dollar amounts - makes it real.

List out all your debts first - you need to see what you're dealing with. Two main approaches: debt avalanche (hit highest interest rates first, saves more cash) or snowball method (knock out smallest balances for quick wins). Personally I'd go avalanche but honestly? Pick whatever won't make you want to give up after two months. Set up a tight budget with minimums plus extra payments, then automate everything so you can't chicken out. Maybe look into consolidating if you can snag better rates. Oh and don't raid your emergency fund unless something's actually on fire.

Most people say 3-6 months of expenses, but it really depends on your job situation. Stable job with good benefits? Three months is probably fine. Self-employed or working somewhere kinda unpredictable? I'd go for six months, maybe more. Personally, I'm paranoid so I keep extra - it just helps me sleep better, you know? Don't calculate based on your whole budget though. Just figure out rent, utilities, groceries, debt minimums. The bare bones stuff. Start with whatever you can swing. Even like $500 beats having nothing when your car decides to die on a Tuesday.

Interest rates mess with basically everything money-related. High rates? Your savings actually earn something decent, but good luck affording that mortgage. When they're low, borrowing gets cheap (perfect for big purchases), though your cash earns like nothing - super annoying. Bonds get hammered when rates rise, and stocks become less appealing since safer investments finally pay decent returns again. I'd focus on paying off variable debt when rates climb up. Oh, and definitely lock in fixed loans when rates drop. My cousin waited too long last year and totally regretted it.

Dude, just automate that retirement stuff first - like 10-15% straight to your 401k before you can spend it on random things. I learned this the hard way lol. After that's handled, figure out what's left for your emergency fund and house savings. Write down everything you want to save for and give each thing a percentage. It's honestly like meal planning - you gotta prioritize the important stuff but can't ignore everything else. My coworker does this thing where she pretends retirement contributions don't exist in her paycheck. Works pretty well since you can't miss money you never see.

Honestly, those financial reviews are what separate the people who actually hit their goals from those who just hope things work out. Life throws curveballs constantly - promotions, breakups, surprise expenses, whatever. Without checking in regularly, you're basically flying blind. I do a quick check every quarter when something big changes, then go deeper once a year. It's actually pretty cool watching your net worth grow over time (assuming it does, lol). The trick is setting up calendar reminders now while you're thinking about it. Otherwise you'll forget and suddenly it's been three years since you looked at anything.

Oh man, personal finance apps are honestly such a lifesaver! I used to be drowning in spreadsheets but now everything syncs automatically with my bank accounts. Mint and YNAB are solid choices - they'll track your spending and actually show you where all your money disappears to each month. You'll get alerts when you're about to blow your budget too. The categorizing thing is super helpful for spotting patterns. Just pick one that doesn't make you want to throw your phone and actually use it for a few months. I was skeptical at first but it really does help with setting realistic goals and staying on track.

Honestly, just stick with index funds and ETFs to start - they're cheap and you get hundreds of companies automatically. Individual stocks are fine if you actually want to research stuff, but most people (myself included) are lazy and do better buying the whole market anyway. Definitely max out your 401k match first though, that's just free money sitting there. REITs are cool for real estate exposure without dealing with tenants calling about broken toilets. Start with broad market funds in your IRA or 401k, then get fancy later once you've got that foundation down.

So first thing - get that emergency fund sorted, like 3-6 months of expenses saved up. Trust me on this one. Spread your investments around too, don't dump everything into one stock or crypto (learned that the hard way). Insurance is boring but necessary - health, disability, life insurance if you've got kids or whatever. Oh and rebalance your portfolio every so often, maybe quarterly? Think about what could actually mess up your money goals first, then figure out how to protect against that stuff. Diversification really does work, even though it sounds like financial advisor BS.

Honestly, I'd hit that 401(k) hard first - especially if your company matches, because free money is free money. After that, maybe look into Roth conversions when you're having a lighter income year. HSAs are pretty sweet too if you've got a high-deductible plan - they're like triple tax-free which is nuts. You can also do tax-loss harvesting with your regular investments. Oh, and timing stuff helps - like if you're gonna donate to charity anyway, bunch it all in one year instead of spreading it out. But yeah, start with maxing that 401(k).

Honestly, big life stuff just turns your money plans upside down. Marriage means juggling two people's financial baggage - and trust me, everyone's got some. Then kids hit and suddenly you're hemorrhaging cash on daycare and college funds you never thought about. Career changes are brutal too because your income might tank or bounce around like crazy. I swear, what made sense financially last year becomes totally irrelevant after one major event. Don't wait for some arbitrary annual review - tweak your budget whenever life throws you a curveball. Your future self will thank you.

Dude, the worst thing you can do is be super vague about what you want. "Save more money" means nothing - say "$500/month for emergencies" instead. Also don't obsess over just paying off debt OR just investing, you need both happening. Oh and those random expenses like when your car decides to break down right before Christmas? Yeah, budget for that stuff because it WILL happen. Honestly, just write down real numbers for your goals first, then actually see where you money's going each month. That's like step one before doing anything else.

-

Informative design.

-

Easily Understandable slides.

-

Content of slide is easy to understand and edit.

-

Top Quality presentations that are easily editable.

-

Unique design & color.