Subprime mortgage crisis powerpoint presentation slides

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Introducing Subprime Mortgage Crisis PowerPoint Presentation Slides. The presentation highlights the impact of the financial crisis of the year in percentages. Take the advantage of our ready-to-use PPT template to showcase fall in housing prices, unemployment, etc. during a crisis. The impact of a great recession on investment banks is also discussed in this presentation. This content-ready slide design also illustrates the significant financial bubble burst of financial years. Highlight the cost of the financial crisis and its key members. The effects of the crisis on the economy of the US can be effectively discussed using our PPT theme. Showcase how the crisis started spreading in various other parts of the country with the use of this PPT visual. Depict how CDO customers protect themselves during the recession. Explain the effect of subprime in many countries with this PPT theme. Further, describe the current scenario after a decade of a financial crisis in the US. Explain fed tapering, quantitative easing, etc. effectively by using this PPT slideshow. At last, the presentation discusses the vision, mission, and goals of the company.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

Slide 1: This title slide introduces the Subprime Mortgage Crisis. Add the name of your company here.

Slide 2: This slide presents the 2008 Financial Crisis Impact Explained in Numbers.

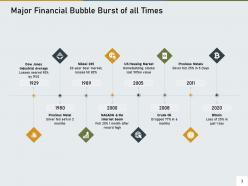

Slide 3: This slide presents the Major Financial Bubble Burst of all Times.

Slide 4: This slide presents the Impact of the Great Recession on Investment Banks.

Slide 5: This slide presents the 2008 Financial Crisis Cost.

Slide 6: This slide presents the Key Figures of the Crisis.

Slide 7: This slide presents Before the Beginning.

Slide 8: This slide presents What Happened then?

Slide 9: This slide presents How did it Spread?

Slide 10: This slide presents How did those who Bought CDO Protect themselves?

Slide 11: This slide presents the Beginning of the End.

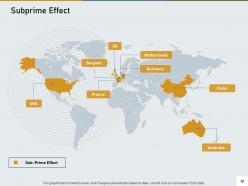

Slide 12: This slide presents the Subprime Effect.

Slide 13: This slide presents the Major Bailout Packages.

Slide 14: This slide presents the Banks that have Paid Billions of Dollars in Fine.

Slide 15: This slide presents After a Decade – Current Scenario

Slide 16: This slide presents the Fed Tapering.

Slide 17: This slide presents the Quantitative Easing.

Slide 18: This is the Subprime Mortgage Crisis Icons Slide.

Slide 19: This slide introduces the Additional Slides.

Slide 20: This slide provides the Mission for the entire company. This includes the vision, the mission, and the goal.

Slide 21: This slide shows the members of the company team with their name, designation, and photo.

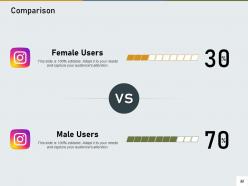

Slide 22: This slide shows the Comparison between the percentages of male and female Instagram users.

Slide 23: This slide presents the overall Target of the company as well as smaller targets within that main Target.

Slide 24: This is a slide with a 30 60 90 Days Plan to set goals for these important intervals.

Slide 25: This slide presents the Financial with a data’s numbers at minimum, medium, and maximum percentage.

Slide 26: This slide is a Timeline template to showcase the progress of the steps of a project with time.

Slide 27: This is a Thank You slide where details such as the address, contact number, email address are added.

Subprime mortgage crisis powerpoint presentation slides with all 27 slides:

Use our Subprime Mortgage Crisis Powerpoint Presentation Slides to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Subprime mortgage crisis

So basically banks were handing out mortgages to anyone with a pulse, even people who obviously couldn't pay them back. Then they got clever and packaged all these garbage loans into fancy investment products that nobody really understood. Rating agencies were supposed to catch this stuff but they were getting paid by the same banks, so... yeah. Mortgage brokers just wanted their commissions. The whole system was built on pretending everything was fine. My dad always said if something sounds too good to be true, it probably is – and man, cheap money for everyone definitely was.

So basically when housing crashed, banks got completely screwed because they were sitting on all these mortgage securities that became toilet paper overnight. Lehman Brothers just died. Others needed huge bailouts to stay alive. The whole thing went global since banks had been selling this garbage worldwide - honestly such a predictable disaster in hindsight. Investment banks, regular banks, insurance companies, they all couldn't get cash when they needed it. That's why now there's way stricter rules about how much money banks have to keep around and all those stress tests.

Yeah, government policies were a huge factor. Banks got pushed to lend in underserved areas through the Community Reinvestment Act. Fannie and Freddie kept buying more subprime mortgages to hit their affordable housing targets - honestly pretty reckless looking back. Regulators just ignored all the sketchy lending going on. Interest rates stayed crazy low too, which totally inflated the bubble. I mean, housing policy shouldn't trump basic common sense about who can actually pay back loans, right? Watch for that same pattern today.

Dude, those adjustable-rate mortgages were such a scam. They'd hook people with crazy low rates at first - like 2% or whatever. Then after a couple years? Your payment would literally double overnight when the rate jumped up. Most people had no clue this was coming and just couldn't afford it anymore. Honestly the worst part was that banks totally knew this would happen but didn't care since they'd already sold the loans to other investors. When everyone started defaulting at once, that's what crashed everything. My uncle got burned by one of these back in '07. Just stick with fixed rates, trust me.

Ugh, it was brutal. Millions of people lost their homes when those "introductory" rates jumped up and suddenly they couldn't afford payments anymore. Lenders were basically handing out loans to anyone, hiding fees and using confusing terms people didn't get. Credit scores got wrecked, families went bankrupt, lost everything they'd saved for. The worst part? They deliberately went after communities that were already struggling. I swear some of these lenders knew exactly what they were doing. Always get someone who knows mortgages to look over anything before you sign - seriously.

So basically, banks figured out they could package up mortgages and sell them to investors - which totally screwed up their incentives. Why be picky about borrowers when you're just gonna offload the risk anyway? They started saying yes to pretty much everyone because pumping out more loans meant more money. This whole mess spread bad debt everywhere since these mortgage bundles got sold globally. Honestly, the "slice and dice" thing was brilliant until it wasn't. If you're ever looking at anything mortgage-backed, just check what's actually underneath first.

Dude, those credit agencies totally screwed everyone over. They slapped AAA ratings on mortgage securities stuffed with garbage subprime loans. Why? Banks were literally paying them to rate their own products - talk about sketchy. Their models were ancient and couldn't handle a housing market collapse. Honestly, it's wild how they got away with such lazy research. So yeah, always check who's funding these ratings before you trust them. Also dig into how they actually calculated the scores, because apparently nobody was doing that back then.

So basically, lenders figured out they can't just throw money at anyone without checking if they actually have income. Wild concept, I know. Housing prices don't magically go up forever - who would've thought? Banks also learned that selling off sketchy loans doesn't make the risk disappear. Now they actually stress test their portfolios against different scenarios instead of just hoping for the best. Bottom line: verify income properly, don't trust credit scores alone, and bubbles always pop eventually.

So basically what happened was like dominoes falling everywhere. US mortgage securities went bad, but banks globally had bought into this stuff too. Credit markets totally froze because nobody knew who was screwed - honestly, it was chaos. Lehman Brothers went under, stock markets crashed worldwide, and Iceland's whole banking system just... died. Modern finance is so connected that our housing mess became everyone's nightmare. I always think about this when people talk about "safe" investments - everything's way more linked than it looks.

So after 2008 they actually did some stuff. Dodd-Frank made banks hold way more capital - like a safety net. The Volcker Rule basically said "no more gambling with your own money." Also we finally got the Consumer Financial Protection Bureau, which honestly took forever. Credit agencies can't just slap AAA ratings on trash anymore either. Oh and if you're buying a house now? Prepare for paperwork hell - they stress test everything. Banks hate it but whatever, maybe don't crash the economy next time.

Ugh, it was so uneven. Black and Hispanic families got absolutely destroyed - foreclosure rates were like 2-3x higher than white neighborhoods. Banks literally targeted these communities with garbage subprime loans, even steering people into worse deals when they could've qualified for better rates. Single moms got hit hard too since they ended up with more of those risky mortgages. The wealth gap just exploded after that. It's wild how much of today's housing mess traces back to this unequal disaster tbh.

Yeah so journalists totally missed the early warning signs - they were blindsided like everyone else tbh. Once shit hit the fan though? Media went into overdrive with nonstop "FINANCIAL COLLAPSE" coverage that honestly made everything worse. Bank runs got uglier because people were glued to these panic-inducing headlines 24/7. It created this weird cycle where fear just kept feeding more fear. Pretty wild how coverage can either chill markets out or send them completely off the rails - definitely something to study if you're into crisis stuff.

Dude, the subprime crisis was brutal for jobs. Unemployment jumped from like 5% in 2008 straight to over 10% the next year - hadn't been that bad since the Great Depression. Construction workers obviously got destroyed first when housing tanked, but then it spread everywhere. People stopped spending, credit froze up, and companies just started mass layoffs across every industry. Housing markets are honestly pretty good at predicting what's gonna happen with jobs overall - something worth watching if you're thinking about investments or whatever.

Dude, the 2008 crisis absolutely wrecked homeownership for like a decade straight. We're talking rates falling from 69% down to 63% - that's huge. Young people and minorities got completely screwed because banks tightened up lending so much. I mean, can you blame people for being terrified of buying after watching entire neighborhoods get foreclosed on? Things have bounced back a little lately, but we're still not where we were before. Honestly changed how most Americans think about owning vs renting. Something to consider if you're thinking about the market long-term.

So after 2008, regulators basically said "never again" and went nuts with new rules. Dodd-Frank came in 2010 - that's what created the Consumer Financial Protection Bureau. Now lenders actually have to check if you can pay back your loan before giving it to you (wild, I know). Banks can't do as much risky trading anymore either. Oh and they have way stricter capital requirements now, plus regular stress tests to make sure they won't collapse. If you're working in finance, this stuff still runs everything today so you'll definitely want to know what applies to your area.

-

Content of slide is easy to understand and edit.

-

The content is very helpful from business point of view.

-

Wonderful templates design to use in business meetings.

-

I discovered this website through a google search, the services matched my needs perfectly and the pricing was very reasonable. I was thrilled with the product and the customer service. I will definitely use their slides again for my presentations and recommend them to other colleagues.

-

Wonderful templates design to use in business meetings.