Business Loan Performance Analysis Dashboard

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

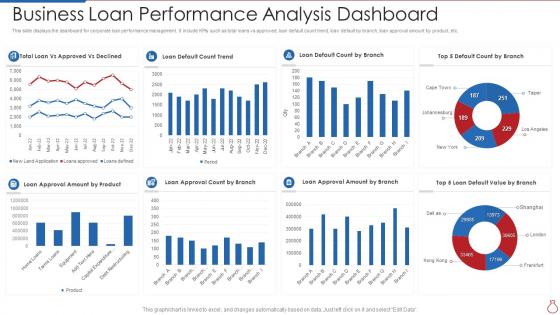

This slide displays the dashboard for corporate loan performance management. It include KPIs such as total loans vs approved, loan default count trend, loan default by branch, loan approval amount by product, etc.

People who downloaded this PowerPoint presentation also viewed the following :

Business Loan Performance Analysis Dashboard with all 7 slides:

Use our Business Loan Performance Analysis Dashboard to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Business Loan

Okay so first thing - get your debt-to-income ratio under 40%, that's what they really care about. Credit score needs to be 680+ obviously. Make sure your cash flow looks solid over the past few years, banks hate when they can't see consistent income. Oh and that debt service coverage ratio thing? Keep it above 1.25 if you can. Honestly, the collateral part trips people up - you need actual equity in the game or they'll just pass. Been there with my cousin's restaurant loan, total nightmare. Pull all these numbers together before you apply though, saves so much headache later.

So basically, banks look at your debt-to-equity ratio to see if you're already drowning in debt. High ratio = red flag for them. They want to see you're not maxed out before handing over more money. Most banks like seeing ratios under 2:1, though some industries naturally run higher - manufacturing comes to mind. The magic number is usually between 1:1 and 1.5:1. If yours is looking rough, pay down some debt first or pump up your equity. Honestly, this one number can kill your chances before you even walk in the door.

So basically your credit history is like your financial report card to lenders. Good credit = better interest rates and loan terms. Bad credit = you're gonna pay more and jump through hoops. Makes sense from their side though - they want proof you actually pay your bills on time before handing over cash. I'd definitely check your credit report first and clean up any mistakes (there's always some random error on there). Your credit score basically tells them whether you're responsible with money or not. Higher score means they'll compete for your business with their best offers.

Look, lenders care way more about whether you can actually pay them back than how pretty your balance sheet looks. They'll calculate your debt service coverage ratio from operating cash flow - you need at least 1.25x coverage, so $1.25 generated for every dollar you owe. Timing issues kill even profitable businesses, which is why they examine your cash conversion cycle closely. Seasonal stuff matters more than most people realize too. Oh, and definitely clean up those cash flow statements beforehand. Have 3-6 months of historical data ready when you apply.

So basically, most lenders want real estate - like your house or commercial property. Business stuff works too (equipment, inventory, whatever). Cash or securities are solid options. Real estate's their favorite honestly, since it's pretty straightforward to price and sell if things go sideways. Oh, and personal guarantees are huge, especially if your business is newer and doesn't have much to show yet. Your collateral usually needs to be worth more than what you're borrowing. Before you even start applying though, make a list of what you actually own. That way you're not scrambling later trying to figure out what you can put up.

Dude, interest rates are killer - they literally multiply your total loan cost. Take $100k over 5 years: at 5% you'll pay around $13k in interest, but at 8%? That jumps to $22k. Nearly ten grand more! Our equipment loan last year was a nightmare because I didn't negotiate hard enough upfront. The longer your loan term, the worse it gets since you're basically paying interest on top of interest. Don't just look at monthly payments either - always calculate what you'll pay total. Trust me, fight for every percentage point you can get.

So basically, amortization schedules are great because you know exactly what you're paying every month - makes budgeting so much easier. The downside? Those early payments are like 90% interest, which is honestly pretty brutal to watch. But knowing your exact payment lets you plan around everything else. I always tell people to plug that fixed payment into their budget first, then figure out the rest. Oh, and if your business has slow seasons, this predictability is a lifesaver since you can prep for those revenue dips. Just pull your schedule and you'll see what I mean.

Oh totally, your industry makes a huge difference. Lenders basically sort sectors into risk levels - tech startups and restaurants get hit with tougher terms because they're seen as risky. Meanwhile healthcare and professional services usually score better rates. Some industries like cannabis? Good luck finding a mainstream lender at all. Others specialize in "high-risk" stuff but you'll pay through the nose for it. They look at your sector's cash flow patterns, how seasonal you are, failure rates - the whole deal. Honestly your best bet is finding lenders who actually get your industry and work with it regularly.

Look, forget the historical stuff that big companies use. Your personal credit score is gonna matter way more since your business probably has zero credit history. Focus on the forward-looking numbers - projected cash flow, how you're acquiring customers, growth rates. Show them your burn rate and runway too. The key thing? Map out exactly where their money's going and what milestones you'll hit. Lenders eat that stuff up. Oh, and definitely explain how the loan fits your growth plan - that's honestly make-or-break for most startup applications.

Look, external stuff controls pretty much all your loan metrics - rates, defaults, approvals, everything. Economy's good? Banks get loose with standards and defaults drop since businesses are crushing it. Things go south though (2008 was brutal), and banks slam on the brakes immediately. Your data will show their panic before you even process what's happening. Unemployment spikes, inflation hits, whole sectors tank - it all pops up in your numbers first. Honestly, tracking leading indicators beats playing catch-up every time. Way better than scrambling after your portfolio's already taken a hit.

So basically, short-term loans are all about cash flow right now - banks check your current ratio, working capital, that kind of stuff. They want proof you can make payments for the next year or two. Long-term financing? Totally different game. Now they're digging into debt-to-equity ratios, profit margins, whether your industry will even exist down the road. It's like the difference between "can you pay me back next month" vs "will I ever see this money again" (which honestly makes sense from their perspective). You'll need recent financials for short-term stuff, but long-term means full business plans and projections.

Look, you can't just throw numbers at them and hope it sticks. Focus on what they actually want to see - debt service coverage ratio, current ratio, cash flow trends. Make a simple dashboard showing past, present, and future. Trust me, loan officers deal with garbage presentations all day, so clean visuals will help you stand out. If you had a rough month or weird dip, explain what happened - don't leave them guessing. Oh, and here's the key part: after each section, spell out exactly what this means for paying back their money. They need that connection made crystal clear.

Look, banks basically want to see you're not gonna default on them. Show realistic revenue growth and cash flow that actually makes sense over your loan period. Don't go crazy with the projections - I've seen people get rejected for being too optimistic. They'll compare your numbers to industry standards anyway, so be conservative. Document everything because they WILL grill you on your assumptions. Short answer? Make it believable. Your forecasts are literally what convince them you're worth the risk, so spending extra time getting the math right is huge.

So LTV ratios are all over the place depending on what you're doing. Real estate? You'll usually see 70-80% because houses hold value pretty well. Manufacturing equipment drops to like 50-60% since that stuff loses value fast. Restaurants get screwed - maybe 40% if they're lucky because who wants to buy used pizza ovens, right? Tech companies have it even worse with all their intellectual property that you can't exactly repossess. Before you apply anywhere, just look up what's normal for your industry so you don't get your hopes up for some crazy high amount.

So current ratio is just current assets divided by current liabilities - shows if they can pay short-term debts. You want above 1.0, obviously. Below 0.8? I'd be sweating. But here's the thing - don't just stare at one number. Check what's normal for their industry first. Then look at trends over a few quarters. If it's been dropping steadily, that's when you really need to worry about their cash situation. Oh and honestly, I've seen way too many companies with decent ratios still struggle because timing matters more than the math sometimes.

-

Illustrative design with editable content. Exceptional value for money. Highly pleased with the product.

-

The team is highly dedicated and professional. They deliver their work on time and with perfection.