Investment Advisory Powerpoint Presentation Slides

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

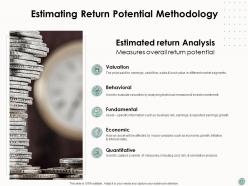

When an advisor provides financial services to the clients to improve its monetary conditions is often referred to as investment advisory. They offer strategic investment advice, realistic budget planning, and creative solutions to manage the organization’s economy. The main objective of an investment advisor is to preserve and build the value of the client’s assets. However, choosing the best financial advisor is very important for a client. To make it easily approachable to the service providers, readymade proposals are made. Pitch your investment plan and land new clients with the help of our topic-specific Investment Advisory PowerPoint Presentation Slides. By using this visually-appealing financial advisory proposal PPT layout, you can design an impressive cover-letter for your landing page that holds the interest of your clients. Take advantage of our eye-catching investment advisory proposal PowerPoint theme to showcase the types of asset classes such as domestic equities, international equities, fixed income, alternative, and bonds. Employ this creatively designed wealth advisory presentation slide to highlight your return potential methodology that involves valuation, behavioral, fundamental, economic, and quantitative methods. Included here are icons and visuals with which you can make your proposal even more attractive yet professional. With the help of this financial advisory proposal PPT slide, you can define the various communication channels that assist your clients in achieving their goals. These channels are PDF & video, market discussions & updates, website, mobile app, and social network. By using this investment advisory proposal PPT slide, you can explain to your clients how you run a standard financial management company. Use the investment advisory proposal PowerPoint theme to portray the skills and capabilities of your highly-experienced team of financial advisors that help your clients in maintaining their budget. Establish the long-term financial security of your client by downloading our fully customizable investment ppt templates.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

Slide 1: This slide introduces Investment Advisory. State Your Company name and begin.

Slide 2: This slide displays Cover Letter.

Slide 3: This slide displays Proposal Outline.

Slide 4: This slide showcases Project context & objectives.

Slide 5: This slide displays Project Context & Objectives.

Slide 6: This slide depicts Investment Details.

Slide 7: This slide showcases How we Propose to Answer your Questions?

Slide 8: This slide showcases Proposal Outline.

Slide 9: This slide shows Types of Asset Class we Invest in.

Slide 10: This slide represents Our Investment Strategy.

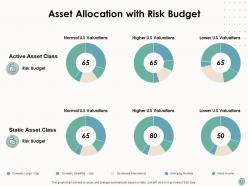

Slide 11: This slide showcases Asset Allocation with Risk Budget.

Slide 12: This slide displays Proposal Outline.

Slide 13: This slide showcases Holdings Summary. This slides mentions details of all investment portfolio for the existing customer

Slide 14: This slide presents Allocation Overview.

Slide 15: This slide shows Proposal Outline.

Slide 16: This slide showcases Estimating Risk Potential Methodology.

Slide 17: This slide depicts Estimating Return Potential Methodology.

Slide 18: This slide displays Proposal Outline.

Slide 19: This slide explains Return on Investment & Fees.

Slide 20: This slide depicts Proposal Outline.

Slide 21: This slide depicts Communication.

Slide 22: This slide displays Proposal Outline.

Slide 23: This is About Us slide to showcase Company specifications.

Slide 24: This slide shows Our Investment Philosophy.

Slide 25: This is Our Team slide with names and designations.

Slide 26: This is Our Team slide with names and designations.

Slide 27: This slide displays Proposal Outline.

Slide 28: This slide represents Client Testimonials.

Slide 29: This slide showcases Case Study.

Slide 30: This slide displays Proposal Outline.

Slide 31: This slide displays Next Steps.

Slide 32: This is Contact Us slide with Address, Email address and Contact number.

Slide 33: This slide is titled as Additional Slides for moving forward.

Slide 34: This is Our Mission slide with Vision, Mission and goals.

Slide 35: This slide displays Roadmap process.

Slide 36: This slide depicts Roadmap process.

Slide 37: This slide depicts Roadmap process.

Slide 38: This slide also depicts Roadmap process.

Slide 39: This slide also depicts Roadmap process.

Slide 40: This is 30 60 90 Days Plan slide.

Slide 41: This slide displays Time Line process.

Investment Advisory Powerpoint Presentation Slides with all 41 slides:

Use our Investment Advisory Powerpoint Presentation Slides to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Investment Advisory

First thing - check they're actually licensed and have fiduciary duty (means they legally have to put you first). Fees matter big time since percentages add up over years, so compare flat rates vs. percentage models. Their investment style should match your risk tolerance too. I always think past performance is kinda BS but still worth checking out their track record. Do they specialize in what you need? Retirement planning is totally different from wealth building. Honestly, just hop on a call with them first - you'll know pretty quick if their communication style works for you or not.

Start with their Form ADV - basically their report card showing fees, credentials, and any sketchy history. FINRA's BrokerCheck is good too for complaints. Honestly, I'd care more about their actual experience than fancy letters after their name, though CFP or CFA doesn't hurt. Make sure their investment style actually fits what you want, not just what sounds smart. The real test? Meet with them and ask how they'd handle your situation. Good advisors explain things clearly without drowning you in jargon. If they can't break it down simply, keep looking.

So diversification is just spreading your money across different stuff so you don't get totally screwed if one thing crashes. Your advisor will mix stocks, bonds, real estate, different countries, industries - the whole deal. It's way more complex than that "don't put eggs in one basket" thing everyone says. The point isn't making crazy returns but getting decent risk-adjusted gains over time. Honestly, most people think they're diversified but aren't really. You should actually look at what you own and see if it's spread out enough.

So basically your advisor will give you some questionnaires and ask how you feel about market swings to figure out your risk tolerance. Conservative people get more bonds, aggressive types get more stocks - pretty straightforward. Your age plays into it too since younger folks can bounce back from losses easier. They'll also look at your goals and timeline. Honestly, the best thing you can do is just be super honest about what financial stuff stresses you out. Like, what would actually make you lose sleep? Once they know that, they can build something that won't have you checking your portfolio at 2am.

Most advisors charge either a percentage of your assets (usually 0.5-2% per year) or hourly/flat fees. Here's the thing - those AUM fees are a real drag since they come out whether you make money or not. Like, if they charge 1%, you literally need to earn that just to break even. Hourly might cost more upfront but could be cheaper if you're not constantly tweaking things. There's also performance-based fees but honestly those are pretty rare. I'd just make sure you know exactly what you're paying - my cousin got hit with all these random charges she didn't expect.

Market trends basically control how advisors build your portfolio. Bull markets? They'll push aggressive growth stuff - tech stocks, emerging markets, riskier bets. Bear markets completely flip that to defensive plays like bonds and dividend stocks. Some advisors definitely overreact to whatever just happened, which is annoying. The good ones actually use historical data to balance current trends with long-term strategy though. What you really want to watch is whether your advisor's just trend-chasing or actually explaining how this stuff fits your specific goals and timeline.

So basically, a fiduciary has to put your money interests first - legally, not just because they're being nice. It's like having someone who's legally required to have your back financially. Most advisors can sell you whatever makes them the most commission, which honestly sucks. But fiduciaries? They'll get in legal trouble if they screw you over for their own benefit. Always ask upfront if they're a fiduciary. Trust me, you want someone who HAS to help you, not just someone who might if they feel like it.

Honestly, robo-advisors are pretty great for handling all the boring stuff - portfolio rebalancing, tax-loss harvesting, basic allocations. I don't miss doing that manually at all. What's cool is they free you up for the stuff clients actually care about. You know, building relationships, complex planning, talking them off ledges when markets go crazy (algorithms suck at that). My friend who's been using one for like two years says it's more like having a really efficient assistant than competition. Start by figuring out what routine tasks are eating your time. Then find tech to automate those first.

So active investing is basically trying to pick winners - higher potential returns but way more expensive fees. Plus your manager might just suck at it. Passive is the opposite: you're buying everything in an index for cheap, getting whatever the market gives you. Here's the thing though - most active managers can't even beat the market long-term, which is honestly pretty embarrassing for them. I'd probably do a mix: stick most of your money in boring index funds, then throw some at active stuff where it might actually matter. Like emerging markets or whatever.

Yeah, good advisors basically bake taxes into everything they recommend. They'll check your bracket and suggest stuff like tax-loss harvesting or putting dividend stocks in your IRA instead of taxable accounts. During low-income years, they might push Roth conversions. Higher earners often get steered toward munis - though honestly the tax code is such a mess that this is where they really prove their worth. Oh, and bring your tax return to meetings! Makes a huge difference for getting advice that actually fits your situation.

Honestly, it's pretty straightforward but a lot of people mess it up. Put your clients first, period. Don't push expensive products just because you get better commissions - I've seen too many advisors go down that road and it never ends well. Be upfront about what you charge and if you have any skin in the game with investments you're recommending. Actually listen to what they want and can handle risk-wise before suggesting anything. Oh, and here's my test: would I tell my sister to do this if she were in the same spot? If not, don't recommend it.

Don't be vague about what you actually want - like saying "I want $80k a year starting at 65" instead of just "comfortable retirement." Tell them how you handle market drops too. Can you sleep through them or do you panic? Oh, and mention big stuff coming up - college tuition, house down payments, whatever. I get that talking money specifics feels awkward, but honestly your advisor can't do much without knowing the real numbers. Write down your top 3 goals beforehand so you don't blank out during the meeting.

Look, macro stuff totally dictates what we tell clients to do with their money. Inflation hits? We're moving away from growth stocks into bonds or defensive plays. Same thing happens when there's recession talk or crazy geopolitical drama going on. Currency swings screw with international picks too - which is honestly annoying but whatever. The whole thing's like chasing a moving target half the time! That's why we keep tweaking portfolio strategy though. Don't freak out when recommendations shift based on these big trends. We're just rolling with whatever's actually happening in the market right now.

Honestly, those regular check-ins are huge for catching stuff before it becomes a real problem. I do them quarterly for most clients - helps spot when their allocations get wonky or investments aren't pulling their weight. Life changes fast too, right? New job, divorce, whatever. Clients eat this stuff up because they feel like you're actually paying attention to them. Oh and document everything - sounds boring but later you can show them exactly how you've helped over the years. Way better than scrambling to fix things after they've already gone sideways.

Keep your regular license requirements current, obviously. But grab specialized certs like CFP or CFA based on your clients. Markets are insane right now - feels like there's new stuff every week. Fintech and ESG questions come up constantly, so stay sharp on those. Tax changes too. Professional associations are worth it for the conferences. Networking's solid, plus you get real-world tips that beat textbooks. I'd budget for two big events yearly. Oh, and don't sleep on the smaller local meetups either - sometimes those are actually more useful than the fancy ones.

-

Good research work and creative work done on every template.

-

Unique research projects to present in meeting.