Finance budgeting powerpoint presentation slides

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Select our professionally designed Finance Budgeting PowerPoint Presentation Slides to improve your profits, reduce costs, and increase return on investments. Keep track of your expenses and revenues with the help of our content ready budget forecast presentation deck. The topic-specific actual vs budget variance PowerPoint complete deck contains a set of self-explanatory templates such as actual cost vs budget, month-wise forecasting, overhead cost analysis, quarterly budget analysis, variance analysis, actual vs target variance, budget vs plan vs forecast, forecast, and projection, etc. Creating and monitoring a budget can keep your business profitable and successful. Manage your finances effectively using the ready-to-use budget presentation slides. Incorporate the professional-looking financial forecasting PPT visuals to showcase steps of developing and planning a budget. Furthermore, the visually appealing corporate budgeting and forecasting PowerPoint templates are also helpful in creating your financial plans. Thus, download the budget variance analysis PowerPoint presentation now and engage your viewers. A hearty chuckle is good for health. Our Finance Budgeting Powerpoint Presentation Slides are firm believers of the fact.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

Slide 1: This slide introduces Finance Budgeting. State Your Company Name and begin.

Slide 2: This slide shows Actual Cost vs Budget in tabular form.

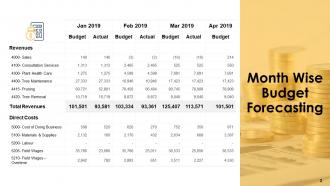

Slide 3: This slide presents Month Wise Budget Forecasting.

Slide 4: This slide displays Overhead Cost Budget Analysis.

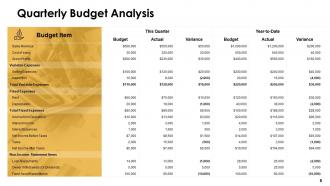

Slide 5: This slide represents Quarterly Budget Analysis in tabular form.

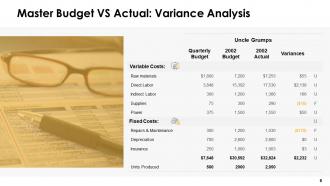

Slide 6: This slide showcases Master Budget vs Actual: Variance Analysis with variable and fixed costs.

Slide 7: This slide shows Actual vs Budget Analysis with categories as original budget, variable cost per unit and flexible budget.

Slide 8: This slide presents Actual vs Target Variance.

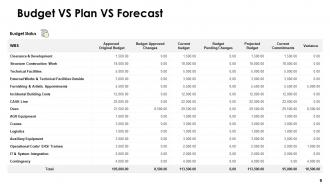

Slide 9: This slide displays Budget vs Plan vs Forecast. You can add data as per requirements.

Slide 10: This slide represents Forecast vs Actual Budget.

Slide 11: This slide showcases Forecast and Projection on monthly basis.

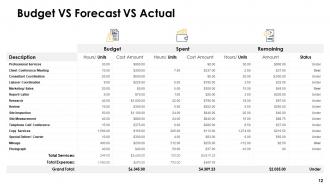

Slide 12: This slide shows Budget vs Forecast vs Actual.

Slide 13: This slide displays icons for Actual Cost VS Budget.

Slide 14: This slide is titled as Additional Slides for moving forward.

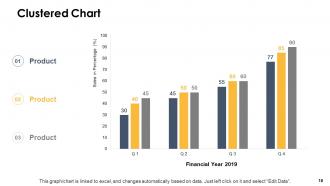

Slide 15: This slide shows Clustered Chart with three products comparison.

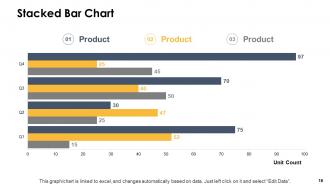

Slide 16: This slide displays Stacked Bar Chart with three products comparison.

Slide 17: This slide is titled as Post It Notes. Post your important notes here.

Slide 18: This is a Financial slide. Show your finance related stuff here.

Slide 19: This is a Venn slide with text boxes to show information.

Slide 20: This is a Location slide with map to show data related with different locations.

Slide 21: This is a Thank You slide with address, contact numbers and email address.

Finance budgeting powerpoint presentation slides with all 21 slides:

Use our Finance Budgeting Powerpoint Presentation Slides to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Finance budgeting

Start with tracking your income first. Then list out fixed stuff like rent and insurance since those won't budge. For variables like groceries and going out, look at what you've been spending lately - that's usually pretty eye-opening honestly. Don't forget emergency fund contributions though, seriously everyone skips that part! Try the 50/30/20 thing as a baseline: half for needs, 30% wants, 20% savings. Whatever's leftover gets split between your regular savings and emergency fund. Track it all for a month so you can see how wrong your estimates were (mine always are).

Honestly, just write down everything you want money-wise and rank what's most urgent. Emergency fund first - trust me on this one, you'll thank yourself later. Then crush any high-interest debt because that stuff bleeds you dry monthly. After that? Retirement savings if your company does matching (free money, duh). House down payment, vacation fund, whatever comes next depends on your life. Don't try to fund everything at once though - you'll make zero progress. Pick maybe 2-3 things max and throw your extra cash at those. Way more effective than spreading it around everywhere.

Honestly, most people think budgeting means you can't have any fun anymore - but that's backwards! It actually lets you spend guilt-free on stuff you care about. You don't need to obsess over every coffee purchase either (that'll just drive you crazy). Small incomes need budgets just as much as big ones do. Maybe more, actually. The whole thing isn't about depriving yourself - it's figuring out what matters to you first. Just start by writing down where your money goes for like a month. Don't worry about fancy apps yet.

Honestly, budgeting apps are a game changer compared to those awful spreadsheets I used to mess with. Mint's free and pretty solid for starting out - it'll connect to your bank and sort your spending automatically. YNAB is another good one if you don't mind paying. The cool part is getting alerts before you blow your budget, plus those visual charts actually show you where all your money disappears to. Way better than just staring at your empty account wondering what happened. I'd definitely try Mint first since it's free, then maybe upgrade later if you get into it.

Okay so I'd definitely go with both automated stuff and checking things yourself. Apps like Mint or YNAB are pretty solid for catching most transactions automatically. But here's the thing - they're not perfect. Like my Target trips always get labeled as "shopping" when half of it was actually groceries, which is super annoying. I keep receipts for maybe a week and double-check against the app. Oh, and if you use cash a lot, that envelope thing actually works. The main thing though? Just pick whatever system and don't abandon it after like two weeks. You need at least a month to see any real spending patterns emerge.

I'd say monthly minimum, but I'm kinda obsessive and peek at mine every two weeks. Life gets crazy fast, you know? Monthly check-ins help you spot when you're blowing through categories or if your budget's totally off from reality. Weekly reviews are clutch if your income's all over the place or you're new to this whole budgeting thing. Oh, and any big life stuff - job changes, moving, whatever - means you gotta redo everything immediately. Pro tip: set a phone reminder or you'll definitely forget like I always do.

Okay so basically an emergency fund is like your "oh shit" money for when life gets messy - car breaks down, surprise medical bill, you lose your job, whatever. Without it, you're either screwing up your regular budget or going into debt every time something happens. I learned this the hard way lol. Start with maybe $1000 if that's doable, but the goal is really 3-6 months of expenses saved up. Just treat it like another bill you pay yourself each month until you get there. Trust me, having that cushion makes such a difference when crazy stuff happens.

Track your income for like 6-12 months first - that'll give you a realistic average to work with. The emergency fund thing is huge though, you'll want at least 6 months saved since your income's all over the place. I do this "bucket" system where I separate fixed costs, random expenses, and savings so I'm not panicking during slow months. When you have a good month, don't go crazy spending it all (I learned this the hard way). Set up automatic transfers right when payments hit your account - seriously, do it before you even think about that money existing.

Track your spending for a month first - you'll be horrified where it all goes. That 50/30/20 rule is actually pretty solid to start with. Look for subscriptions you totally forgot about (we all have them), cut back on takeout, and switch to store brands for boring stuff like detergent. Honestly, meal prep saved me so much money once I got into it. Don't just slash everything though - figure out what actually makes you happy and keep that. Cancel the gym you never use, but maybe keep Netflix if you're always watching. Oh, and try waiting 24 hours before buying random stuff you don't really need.

Track what you're actually spending for a couple months first - don't just guess at numbers. Most people skip the monthly check-ins and then wonder why they're broke by December (learned that one the hard way). Break everything into fixed costs, stuff that changes month to month, and emergency money - maybe 3-6 months worth if you can swing it. Your budget isn't some sacred document you create once. Update it every quarter when things shift. Always compare what you planned vs what really happened so you can catch problems before they get ugly.

Honestly, budgets are game-changers for stress levels. No more lying awake wondering if you can afford rent next month or freaking out when your car needs repairs. You actually know where your cash is going instead of just hoping for the best. Hitting savings targets feels ridiculously good too - like that dopamine hit from crossing stuff off your list. I started by just tracking my big expenses for a few weeks and wow, the relief kicked in fast. Your brain stops doing that constant background worry about money. Just pick 4-5 main categories and see what happens.

Definitely max out that employer match first - seriously, who turns down free money? After that, try hitting 10-15% total for retirement (match included). I get it, that feels like a ton when you're starting out. Honestly though, just begin with whatever you can manage and bump it up 1% whenever you get a raise. Oh, and if you're over 50? Those catch-up contributions are your best friend. The real game-changer is making it automatic so you don't have to think about it every month. Just treat it like your electric bill - something that gets paid no matter what.

Honestly, just track what you're actually spending for like a month or two first - you'll probably be horrified lol. That 50/30/20 rule is decent to start with (needs/wants/savings), but don't stress if your numbers look different. Life's messy. Always throw in some cushion money because your car will break down the second you think you've got everything figured out. The biggest thing? Don't budget for the person you wish you were - budget for who you actually are right now. You can always tweak it later once you see what's realistic.

Look, budgeting is honestly your best shot at actually having money later. Track everything for a month first - yeah it's tedious but you'll be shocked where your cash goes. Then you can cut the dumb stuff and put that money toward savings instead. The real trick? Set up automatic transfers right after you get paid. That way you're saving without even thinking about it. I know it sounds boring as hell, but living below your means is literally how you build wealth. Plus once it's automated, you barely notice.

Budget variance is where I'd start - just the gap between planned vs actual spending. Your variance percentage matters more though, shows if you're consistently off by like 10% or whatever. Cash flow timing can bite you even when your overall budget looks fine. Monthly check-ins are way better than getting blindsided quarterly, trust me on that one. Look at your budget-to-actual ratios across different spending categories. Trends over 3-6 months tell you more than individual bad months. I'm probably too neurotic about this stuff, but it works.

-

Graphics are very appealing to eyes.

-

Design layout is very impressive.

-

Editable templates with innovative design and color combination.