Working Capital Management Excellence Handbook For Managers Fin CD

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

Introducing our Working Capital Management Excellence Handbook for Managers, a comprehensive PowerPoint to enhance financial proficiency. Designed explicitly for seasoned financial practitioners, this module offers advanced insights into Working Capital Optimization, the complexities of the Working Capital Conversion Cycle, and the crucial interaction between Working Capital and Liquidity. Additionally, within these pages, professionals can uncover valuable strategies for making precise decisions in Working Capital Management, refining their Receivable Management processes to achieve optimal cash flow, and attaining outstanding financial results. Remain at the forefront of your field and impact your organizations financial success. Unleash the potential of strategic Working Capital Management with this guide, customized for professionals like you aiming for excellence in the finance domain. Elevate your career and generate tangible results download it today.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

Slide 1: This slide introduces Working Capital Management Excellence Handbook for Managers. State your company name and begin.

Slide 2: This is an Agenda slide. State your agendas here.

Slide 3: This slide shows Table of Content for the presentation.

Slide 4: This slide shows title for topics that are to be covered next in the template.

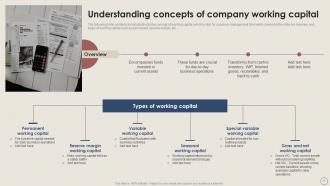

Slide 5: This slide contains an introduction to the concept of working capital, which is vital for business management.

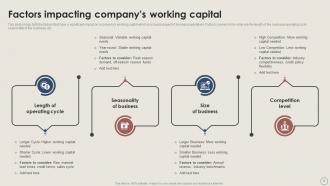

Slide 6: This slide brings forth the factors that have a significant impact on a company's working capital which is a crucial aspect of business operations.

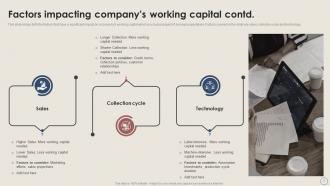

Slide 7: This slide also brings forth the factors that have a significant impact on a company's working capital which is a crucial aspect of business operations.

Slide 8: This slide highlights the significance of working capital in business success. Major points of significance include funds planning, decision-making etc.

Slide 9: This slide delves into the benefits that efficient working capital management can offer to company owners. Major points of benefits covered in the slide.

Slide 10: This slide includes statistics related to working capital management, providing valuable insights for decision-makers.

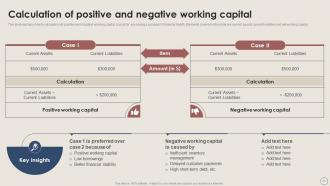

Slide 11: This slide explains how to calculate both positive and negative working capital, crucial for assessing a company's financial health.

Slide 12: This slide shows title for topics that are to be covered next in the template.

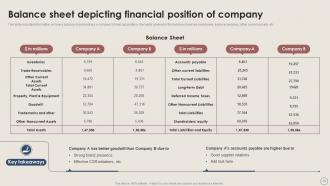

Slide 13: This slide includes information on how a balance sheet portrays a company's financial position. Elements covered in the balance sheet are inventories, trade receivables etc.

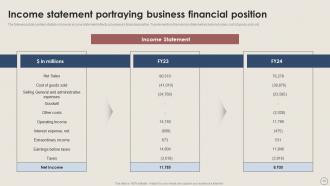

Slide 14: This slide contains details on how an income statement reflects a business's financial position. Top elements in the income statement include net sales, cost of goods sold etc.

Slide 15: This slide focuses on financial metrics that are indicative of a company's financial health. The top metrics covered in the slide are days sales outstanding, days inventory outstanding, etc.

Slide 16: This slide also focuses on financial metrics that are indicative of a company's financial health. The top metrics covered in the slide are return on assets etc.

Slide 17: This slide shows title for topics that are to be covered next in the template.

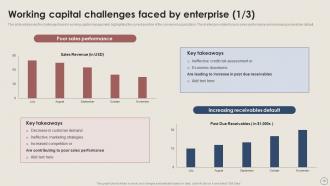

Slide 18: This slide addresses the challenges faced in working capital management, highlighting the current position of the concerned organization.

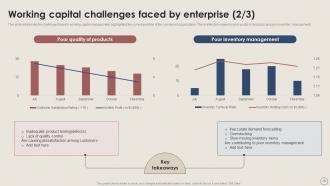

Slide 19: This slide also addresses the challenges faced in working capital management, highlighting the current position of the concerned organization.

Slide 20: This slide presents the challenges faced in working capital management, highlighting the current position of the concerned organization.

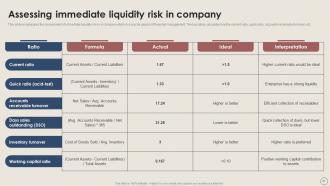

Slide 21: This slide emphasizes the assessment of immediate liquidity risk in a company which is a crucial aspect of financial management.

Slide 22: This slide shows title for topics that are to be covered next in the template.

Slide 23: This slide brings forth an overview of liquidity risk management and its objectives which are crucial for every company.

Slide 24: This slide discusses strategies for securing cash flow through effective liquidity risk management. Top strategies are develop cash flow forecasts, assess insolvency risk etc.

Slide 25: This slide also discusses strategies for securing cash flow through effective liquidity risk management. Top strategies are related to receivables management etc.

Slide 26: This slide shows title for topics that are to be covered next in the template.

Slide 27: This slide brings forth major types of long and short-term considerations that need to be taken care of by the manager.

Slide 28: This slide depicts a process of optimizing working capital for short and long-term success by the business firms. Major steps include assessing the current position, differentiating needs etc.

Slide 29: This slide contains information regarding effective working capital management strategies to be implemented by managers.

Slide 30: This slide shows title for topics that are to be covered next in the template.

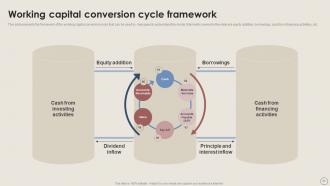

Slide 31: This slide presents the framework of the working capital conversion cycle that can be used by managers to understand the model.

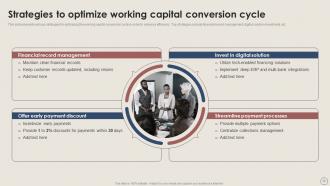

Slide 32: This slide displays various strategies for optimizing the working capital conversion cycle in order to enhance efficiency.

Slide 33: This slide shows title for topics that are to be covered next in the template.

Slide 34: This slide discusses the best practices for improving accounts receivables collection. Top best practices are incentivizing early payments and more.

Slide 35: This slide provides insights into streamlining supplier payment management through automation. Top approaches include spend analytics, vendor relationship management etc.

Slide 36: This slide displays insights into streamlining supplier payment management through automation. Top approaches include sourcing insights, virtual payment etc.

Slide 37: This slide shows title for topics that are to be covered next in the template.

Slide 38: This slide gives insights into how inventory management practices affect a company's working capital. The role of inventory in working capital management relates to cash flow optimization, risk mitigation etc.

Slide 39: This slide includes different types of inventories in working capital management. Top inventories include raw materials, components, work in progress etc.

Slide 40: This slide outlines the process for optimizing inventory performance to boost cash flows. The steps include reassessing inventory strategy, update key performance indicators etc.

Slide 41: This slide shows title for topics that are to be covered next in the template.

Slide 42: This slide includes an overview of tools that assist in working capital optimization that will assist managers for selecting appropriate tool.

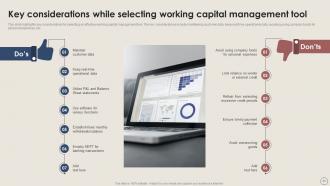

Slide 43: This slide highlights key considerations for selecting an effective working capital management tool. The key considerations include maintaining customer data etc.

Slide 44: This slide presents a matrix for selecting the most suitable working capital management tool. Major elements include software, key features, pricing and customer ratings.

Slide 45: This slide provides insights into the comparison of different working capital finance management tools. The major basis of difference includes top features, pricing etc.

Slide 46: This slide shows title for topics that are to be covered next in the template.

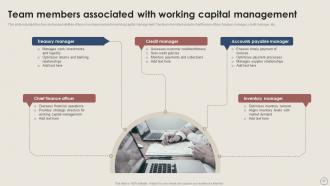

Slide 47: This slide includes the roles and responsibilities of team members involved in working capital management. Top team members include chief finance officer, treasury manager etc.

Slide 48: This slide details the roles and responsibilities of a working capital manager within an organization. Top responsibilities include credit assessment, risk modeling etc.

Slide 49: This slide shows title for topics that are to be covered next in the template.

Slide 50: This slide presents an employee training plan that can be implemented by managers to improve the skill set of the existing workforce and streamline finance management.

Slide 51: This slide brings forth an employee performance, tracking scorecard that can be used by managers to track and monitor the performance of staff.

Slide 52: This slide shows title for topics that are to be covered next in the template.

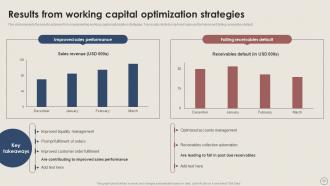

Slide 53: This slide presents the results achieved from implementing working capital optimization strategies.

Slide 54: This slide also displays the results achieved from implementing working capital optimization strategies.

Slide 55: This slide presents the results achieved from implementing working capital optimization strategies. Top results relate to delayed vendor payment, lack real-time information etc.

Slide 56: This slide shows title for topics that are to be covered next in the template.

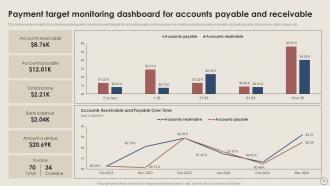

Slide 57: This slide provides insights into a dashboard designed to monitor payment targets for accounts payable and receivable. Key metrics include accounts receivable etc.

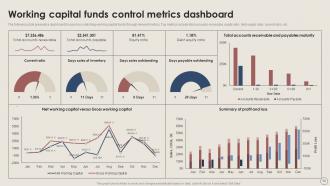

Slide 58: This slide presents a dashboard focused on controlling working capital funds through relevant metrics. Top metrics include total accounts receivable, equity ratio etc.

Slide 59: This slide shows title for topics that are to be covered next in the template.

Slide 60: This slide presents case study explores the impact of negative working capital on a company's profitability. Major elements include an overview, company profile etc.

Slide 61: This slide also presents a case study discusses strategies for optimizing working capital management to enhance overall operations.

Slide 62: This slide presents a case study on Britannia’s working capital management that offers valuable insights to managers. Top elements include challenges, impact etc.

Slide 63: This slide shows all the icons included in the presentation.

Slide 64: This slide is titled as Additional Slides for moving forward.

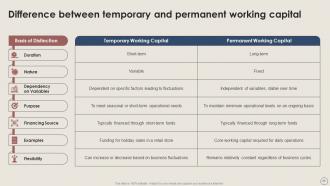

Slide 65: This slide showcases Difference between temporary and permanent working capital with text boxes.

Slide 66: This slide presents Risks of employing excessive working capital with text boxes.

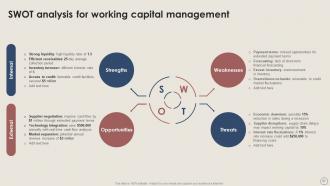

Slide 67: This slide shows SWOT analysis describing- Strength, Weakness, Opportunity, and Threat.

Slide 68: This slide presents Types of working capital management strategies with text boxes.

Slide 69: This is Our Vision, Mission & Goal slide. Post your Visions, Missions, and Goals here.

Slide 70: This is a financial slide. Show your finance related stuff here.

Slide 71: This slide depicts Venn diagram with text boxes.

Slide 72: This slide contains Puzzle with related icons and text.

Slide 73: This is a Thank You slide with address, contact numbers and email address.

Working Capital Management Excellence Handbook For Managers Fin CD with all 81 slides:

Use our Working Capital Management Excellence Handbook For Managers Fin CD to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Working Capital Management Excellence Handbook For

Look at your cash first - you need enough for daily stuff but don't hoard it since idle money is wasted money. Accounts receivable is huge too - basically how fast people actually pay you. Then there's inventory (don't tie up cash in products just sitting around) and payables where you time when to pay suppliers. Honestly, most people mess up the timing part. The goal is getting all four moving together smoothly. I'd start by checking your cash conversion cycle - that's where you'll spot the biggest problems right away.

So working capital management is basically about speeding up your cash conversion cycle - you know, how fast you turn inventory and receivables into actual cash. Manage your inventory better, collect money from customers quicker, and time your bill payments smarter. All that cash that's usually stuck in operations? It gets freed up. Think of it like unclogging a pipe - suddenly everything flows better. The quicker you convert those working capital pieces back to cash, the more liquid you become. I'd honestly start by looking at your current cycle and figuring out what's slowing you down the most.

So inventory turnover is just how quickly you're flipping your stock into actual sales. The faster you move products, the less cash gets trapped sitting around - and trust me, nothing's worse than money just collecting dust on shelves. You'll see better cash flow because you're getting paid quicker and can put that money back to work. Plus it cuts down storage costs and stops you from getting stuck with outdated inventory. I'd check your turnover ratio every month. Compare it against what others in your industry are doing - that's where you'll find the real opportunities to improve things.

Honestly, just make it ridiculously easy for people to pay you. Set up credit cards, ACH, online portals - whatever they want. Send invoices right after you deliver, then automate reminders at 15, 30, and 45 days because people are forgetful as hell. Early payment discounts work too - like 2% off if they pay within 10 days. Track your DSO monthly (that's days sales outstanding if you haven't heard that term). Focus on your biggest slow payers first since that's where you'll actually move the needle on cash flow.

Look, it's all about who has the upper hand in your supplier relationships. Strong suppliers? They'll force you into tight payment windows or even make you pay upfront - total nightmare for cash flow. But flip that around and you can push for 60-90 day terms, maybe score some early payment discounts too. I've seen companies get creative with consignment deals where inventory stays off their books until it sells. Worth checking all your supplier contracts regularly - you might find spots to renegotiate or honestly just diversify so you're not stuck depending on one difficult vendor.

Oh man, seasonality is brutal for cash flow. Your inventory needs go crazy - like if you're in retail, you're stuck buying tons of holiday stock months before you see any money from it. Then suddenly you've got all these receivables sitting there after the rush. Manufacturing hits the same wall, just different timing. I learned this the hard way watching a friend's business almost tank because they didn't prep. You gotta forecast those patterns early and get a credit line set up *before* you're desperate for cash, not after.

Start by digging into your last 12-18 months of cash conversion data - you're looking for seasonal patterns and trends that repeat. Monthly rolling forecasts work way better than annual budgets (which honestly become pretty worthless after like 3 months). Build out three scenarios: best case, worst case, and realistic outcomes for both sales and when customers actually pay you. Track stuff like order backlogs and how your customers have been paying lately - those are solid leading indicators. The real trick is keeping forecasts short-term and constantly updating them with fresh data as it comes in.

Honestly, tech makes such a huge difference with cash flow stuff. Automating invoices and payment collection saves tons of time, plus you get real-time updates on what's coming in and going out. No more digging through spreadsheets to figure out where you stand financially. There are AI tools now that can actually spot which customers might pay late - kind of scary how accurate they are. Your team stops doing boring data entry and can focus on bigger picture decisions. I'd start with digitizing your invoice process first since that's where you'll see results fastest.

So you'll mainly track DSO, DIO, and DPO - basically how fast you collect money, turn inventory, and pay bills. DSO measures collection time (faster = better). With DIO, you want quick inventory turnover but not so fast you're always out of stock. DPO is interesting because paying suppliers slower actually helps your cash flow, just don't piss them off. The magic happens when you combine them: DSO + DIO - DPO gives you the cash conversion cycle. Shorter cycle means money flows back quicker. I'd start by checking industry benchmarks first, then tackle whatever's your biggest mess.

Match your financing to how your cash actually flows. Short-term stuff like lines of credit work great for seasonal inventory or quick gaps. Equipment and permanent working capital? Go long-term. I learned this the hard way - you don't want to be stuck with expensive short-term debt when things get tight. That's a nightmare scenario. Map out your cash conversion cycle first (kinda boring but worth it). Then pick financing that actually lines up with those patterns. The whole point is staying liquid without paying for money you're not using yet.

Map out your current cycle first - you need to see where you're actually bleeding time. Get customers paying faster by offering early payment discounts or tightening up those payment terms. Inventory's usually the biggest cash killer, so work on just-in-time ordering and better forecasting. Don't let dead stock pile up. With suppliers, flip it around - ask for longer payment terms but keep those relationships solid. The whole game is collect quick, stock less, pay slow. Honestly, most businesses don't realize how much cash they've got tied up unnecessarily. Start with the biggest bottleneck you find.

Dude, economic shifts mess with working capital big time. Inflation hits? Hold less cash but buy inventory before prices jump. Higher interest rates make borrowing expensive, so you'll want to speed up that cash conversion cycle. The tricky part is customers start paying slower when times get uncertain, while suppliers want their money faster - honestly feels like you're getting squeezed from everywhere. I'd check these indicators weekly if I were you. Build some wiggle room into your strategy because this stuff changes constantly and you don't want to get caught off guard.

Think of risk management as your cash flow insurance policy. You'll want to check credit risks before giving customers loose payment terms - learned that one the hard way! Also watch your inventory so you don't get stuck with a warehouse full of stuff nobody wants. Supply chain hiccups can really mess with your timing too. Build some cushion into your working capital based on how much risk you can stomach. Oh, and definitely keep an eye on those receivables aging reports and inventory turnover numbers. They'll save you from nasty surprises down the road.

Build up a cash cushion first - like 3-6 months of expenses sitting there. Banks are weird, they'll throw credit lines at you when you don't need money but ghost you when you're desperate. So get those lines set up now while things look decent. Rolling forecasts help you see patterns coming, and factoring can get you quick cash if needed. Honestly, diversifying customers is huge - you don't want to be screwed if your biggest client bails. Same with funding sources. My old boss learned this the hard way during 2008.

Look, cash flow is literally everything for your business - without it, you're dead in the water. Managing your working capital well means you're not tying up tons of money in inventory or waiting forever to collect payments. I've watched profitable companies go under just because they couldn't manage this stuff properly. It's honestly pretty scary how fast it happens. Track your cash conversion cycle every month - sounds boring but it shows you exactly where money gets stuck. Once you get this right, everything else becomes way more predictable. You'll have cash for actual growth instead of constantly stressing about paying bills.

-

Very unique, user-friendly presentation interface.

-

SlideTeam is a great place for PPT templates. They have many templates on a single topic. It has made my life a lot easier.