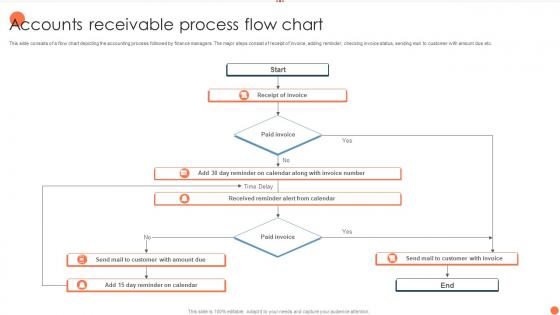

Accounts Receivable Process Flow Chart

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

This slide consists of a diagrammatical representation of financial accounting process followed by finance personnel. The elements are preparation of source documents, journal vouchers, general ledger, collect account balances, adjust trial balances etc.

People who downloaded this PowerPoint presentation also viewed the following :

Accounts Receivable Process Flow Chart with all 6 slides:

Use our Accounts Receivable Process Flow Chart to effectively help you save your valuable time. They are readymade to fit into any presentation structure.

FAQs for Accounts Receivable

Start by mapping out what you're doing now - that'll show you where things are falling apart. You need solid invoicing, aging reports, and clear credit policies. But honestly? Most companies totally blow it on follow-up, which is crazy since that's where you actually get paid. Set up automated reminders and track all your customer conversations in one place. Keep an eye on DSO and collection rates too - they're like early warning signs. Oh, and don't try to fix everything at once. Pick the messiest part first and work from there.

Honestly, tighten up who you approve for credit from the start - saves so much headache later. Get those invoices out the door right after delivery, then set up automatic reminders every 30 days. Some people genuinely just forget to pay, which is wild but whatever. Early payment discounts work great too - like 2% off if they pay within 10 days. Make paying super simple with different payment options. Don't be shy about putting sketchy accounts on credit hold, and check your aging reports weekly so problems don't snowball into disasters.

Honestly, tech has made AR so much easier. You can automate invoicing and payment tracking instead of doing everything manually - total lifesaver. Cloud systems let you send invoices instantly, set up recurring billing, and customers can pay online. There's even AI now that predicts which accounts might not pay (which is kind of wild if you ask me). Everything syncs with your accounting software too, so no more entering the same data twice. The real win? You'll actually have time for strategy and relationship stuff instead of drowning in paperwork. Start with automating whatever you do most often.

Start by pulling their credit reports from Experian or D&B - basic stuff but crucial. Their payment history with other vendors tells you everything. Financial statements are where I spend most of my time though, especially cash flow and debt ratios. Those trade references? Actually call them. Most people just collect the info and never follow up, which is honestly a waste. Set credit limits based on what you discover, and don't be afraid to ask for deposits from sketchy clients. Oh, and build yourself a simple scoring system - saves you from second-guessing every decision later.

Honestly, just get those invoices out the door right away - don't sit on them like I always do with my own stuff. Make everything super obvious: payment terms, line items, due dates. The whole nine yards. Setting up automated reminders is clutch because manually chasing people down sucks. Oh, and definitely give people multiple ways to pay - ACH, cards, whatever. Removes all those stupid excuses about "oh I can't pay this way." Automated invoicing software will change your life if you're still doing everything manually. Trust me on this one.

Okay so first thing - document absolutely everything. Emails, calls, whatever evidence you have. Assign someone specific to handle disputes or they'll just vanish into the void (seriously, I've watched invoices sit in inboxes for like 4 months). Make templates for the common stuff to save time, and always give yourself deadlines. The follow-up part is huge though - customers get way less angry when you actually tell them what's happening. Oh, and audit your current disputes first to figure out where things are getting stuck. That'll show you the real problem areas.

Honestly, DSO is your best friend here - shows how long you're waiting to get paid. I'd also check your collection effectiveness index monthly (basically what % you actually collect vs what's owed). Aging reports are clutch too since they break everything into 30/60/90+ day buckets. Bad debt ratio sucks to track but you gotta know what you're writing off. Pull these monthly and compare quarter trends - way easier to catch problems early. Oh, and aging reports literally save me so much time figuring out where to focus collection efforts first.

Dude, AR automation is a game changer for cash flow. Once you automate invoice generation, payments start rolling in way faster - that's honestly where I'd start since it has the biggest impact. No more waiting around for someone to manually send stuff out or chase down late payments. The system just handles it all automatically, even processes payments at like 2am if someone wants to pay then. You'll actually see who owes what instead of guessing. My buddy's company cut their payment time in half just by automating reminders alone. It's basically like hiring someone who works around the clock but doesn't need coffee breaks.

Ugh, AR issues are the worst. Late payments are probably killing you, plus all those disputed invoices and data entry mistakes. Customers love to play dumb about invoices they definitely received. Automate your invoicing if you haven't already - seriously, it'll save your sanity. Set up payment reminders that go out automatically. Make your payment terms super clear from day one. Here's something that actually works: offer like 2% off for early payment. People are weirdly motivated by tiny discounts. Oh, and make sure your invoices aren't confusing - include all the details they need. Stay ahead of problems instead of always putting out fires.

Honestly, data analytics is a game changer for this stuff. Pull your payment history and you'll see patterns - like customers who always pay in 15 days vs those who drag it to 45. I'd start by just dumping everything into Excel first before buying expensive software. You can predict who's gonna be late and focus your energy there instead of bugging the reliable ones. Risk levels become super obvious once you sort customers by behavior. Oh, and some tools actually predict your cash flow from outstanding invoices - saw this at my last job and it was wild how accurate it got.

Honestly, your CRM is a game-changer for collections. You get the whole picture - payment history, how they like to communicate, all that relationship stuff in one spot. Makes you way smarter about your approach instead of just blasting everyone with the same boring dunning letters (which nobody reads anyway). Set up some automated follow-ups and actually track what works with different customers. The relationship data tells you when to push hard vs when someone might need a payment plan. I've seen collection rates jump pretty significantly when people connect their CRM to their AR workflow. Plus customers don't hate you as much.

Start with friendly emails or calls - don't go nuclear right away. Most people aren't trying to screw you over, they're just dealing with their own mess. Gradually get more formal if they keep ignoring you. Payment plans work surprisingly well since customers feel like you're working with them instead of against them. Document everything and set deadlines, but honestly? The respectful-but-persistent approach beats being a hardass every time. Keep following up consistently. Leave room for them to explain what's going on - sometimes there's a real reason behind it.

Bad debts mess with your bottom line in two ways - they tank your net income when you write off uncollectable receivables, and they squeeze your cash flow since you're not actually getting paid for those sales. Honestly, it's one of those things that can sneak up on you fast. Your balance sheet starts looking sketchy to lenders too because high bad debt screams "we don't know how to pick good customers." I'd pull those aging reports and maybe tighten up who you're extending credit to. Better to be picky upfront than deal with collections headaches later.

Honestly, most small businesses screw this up by waiting forever to send invoices - bill immediately after delivery! Get your payment terms crystal clear from day one. Wave or QuickBooks Simple Start are solid for automated reminders without breaking the bank. Here's what works: friendly nudge at 15 days, firmer tone at 30, then actually pick up the phone at 45. Early payment discounts help too - like 2% off if they pay within 10 days. People love saving money, even if it's just a few bucks. Stay consistent with whatever system you pick, even if you're doing everything manually at first.

Yeah, AR's getting crazy automated now. Companies are letting AI handle invoice processing, payment reminders, even credit decisions - which honestly still feels a bit weird to me. Real-time analytics means you can see cash flow issues instantly instead of waiting weeks for reports. Most customers expect tons of payment options too now. The predictive stuff is wild though - it'll flag invoices that might go overdue before they actually do. Everything's moving toward touchless processing. I'd say look at whatever you're doing manually first. That's where you'll get the best bang for your buck with these tools.

-

“There is so much choice. At first, it seems like there isn't but you have to just keep looking, there are endless amounts to explore.”

-

Presentation Design is very nice, good work with the content as well.