Fixed income securities powerpoint presentation slides

Try Before you Buy Download Free Sample Product

Impress Your

Impress Your Audience

Editable

of Time

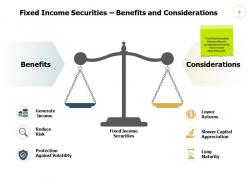

We are introducing Fixed Income Securities PowerPoint Presentation Slides, which helps to make payments of a fixed amount. With the help of the bond market PPT template, you can showcase the various types of marketing securities. If you want to categorize the bond and fixed income securities separately, then use this financial income investment PowerPoint presentation complete deck. You can describe the benefits such as generating income, reducing risk, and protection against volatility using this PPT visual. There are convertible securities as well, which you can highlight with the help of the forwarding rate agreements PowerPoint presentation template. This inflation swaps PPT slides helps you to differentiate between call and put warrants. With the help of our professionally designed interest rate swaps PowerPoint presentation deck, you can generate a table that includes current assets, period returns, and a class of top-performing securities. By using fixed income and leverage securities PPT template, you can classify the various financial leverages. Therefore, download this ready-to-use credit default swaps PowerPoint presentation slides and compute the overall sales revenue.

People who downloaded this PowerPoint presentation also viewed the following :

Content of this Powerpoint Presentation

Slide 1: This slide introduces Fixed Income Securities. State Your Company Name and begin.

Slide 2: This slide shows Contents of the presentation.

Slide 3: This slide presents Marketable Securities Overview describing money market securities, capital market securities, Derivatives and indirect investment.

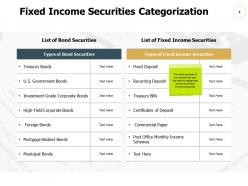

Slide 4: This slide displays Fixed Income Securities Categorization with the help of tables.

Slide 5: This slide showcases the benefits and considerations that the fixed income securities yield.

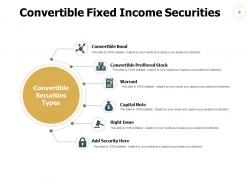

Slide 6: This slide represents Convertible Fixed Income Securities such as- Convertible Preffered Stock, Right Issue, Warrant, Capital Note, Convertible Bond etc.

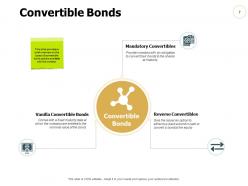

Slide 7: This slide shows Convertible Bonds describing types of convertible bond options available to the investor.

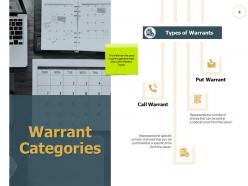

Slide 8: This slide presents Warrant Categories describing call warrant and put warrant briefly.

Slide 9: This slide displays Convertible Preffered Stocks such as- Participating Preferred, Cumulative Preferred, Convertible Preferred, Preference Preferred, Prior Preferred.

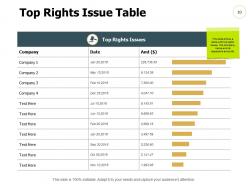

Slide 10: This slide represents Top Rights Issue Table with company name and amount.

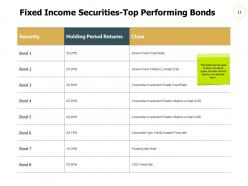

Slide 11: This slide showcases Fixed Income Securities-Top Performing Bonds describing bond types, its class and its returns in a tabular form.

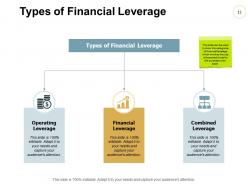

Slide 12: This slide shows Types of Financial Leverage such as- Operating Leverage, Financial Leverage, Combined Leverage.

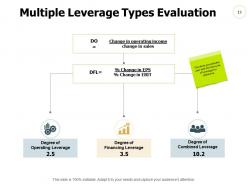

Slide 13: This slide presents Multiple Leverage Types Evaluation with formulas.

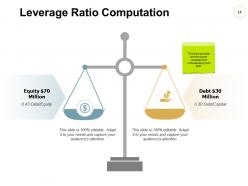

Slide 14: This slide displays Leverage Ratio Computation including equity and debt.

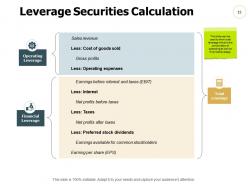

Slide 15: This slide represents Leverage Securities Calculation showing total leverage which is the combination of operating as well as financial leverage.

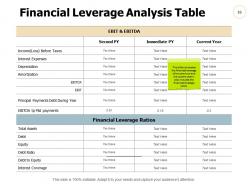

Slide 16: This slide showcases Financial Leverage Analysis Table of previous and current year.

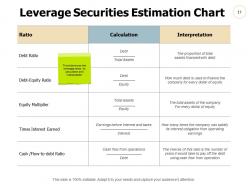

Slide 17: This slide shows Leverage Securities Estimation Chart with leverage ratios , its calculation and interpretation.

Slide 18: This is Our Mission slide with related imagery and text boxes.

Slide 19: This is a Comparison slide to state comparison between commodities, entities etc.

Slide 20: This is Our Goal slide. State your goals here.

Slide 21: This is a Puzzle slide with text boxes.

Slide 22: This is a Thank you slide with address, contact numbers and email address.

Fixed income securities powerpoint presentation slides with all 22 slides:

Indulge in a bit of humour with our Fixed Income Securities Powerpoint Presentation Slides. Drive home your ideas with a grin.

FAQs for Fixed income securities

So fixed income stuff is basically IOUs - bonds, CDs, treasury bills where you loan money out and get steady interest payments back. Your principal comes back when they mature too. Stocks make you a business partner sharing all the crazy ups and downs, but bonds are more like playing banker with predictable cash flows. Yeah, you're still dealing with credit risk and interest rate swings, but honestly it's way less stressful than watching your portfolio bounce around with market drama. Perfect for when you want something stable mixed in with your other investments.

So there's government bonds like Treasuries, corporate bonds, municipal bonds, and agency securities. CDs and commercial paper work for short-term needs. Mortgage-backed securities too if you're feeling adventurous. Municipal bonds can save you a ton on taxes if you're in a higher bracket - honestly wish I'd known that sooner. Corporate stuff pays more but comes with extra risk compared to government bonds. It really comes down to how much risk you can stomach and your timeline. I'd figure out what duration makes sense first, then worry about credit quality from there.

So bond prices and interest rates are basically enemies - when one goes up, the other tanks. Picture you're stuck with a 3% bond but suddenly everyone's getting 5% on new ones. Nobody wants your crappy bond unless you slash the price, right? Duration is this number that shows how much your bond gets hammered when rates move 1%. Longer bonds get hit way harder too, which honestly seems unfair but whatever. Just something to think about when you're picking bonds - rate changes can really mess with your portfolio if you're not careful.

Credit ratings basically tell you how sketchy a bond is - the worse the rating, the higher yield you'll demand. AAA bonds are rock solid so they pay less, while junk bonds have to offer way more to get anyone interested. It's like the market's quick way to judge if you'll actually get paid back. Though honestly, after 2008 I don't trust ratings blindly anymore - those agencies screwed up pretty bad. The rating gives you a starting point for how much extra yield to demand over Treasury bonds. Just don't rely on it completely, do your own homework too.

So credit risk is probably the biggest thing - basically, can the company actually pay you back? Check their credit rating first. Bond prices move opposite to interest rates, which is annoying but predictable. Duration shows how much your bond will swing when rates change - longer duration = more drama. You also gotta think about liquidity (how easy it is to sell) and inflation slowly eating your returns. I know it sounds overwhelming but honestly most of this stuff you can find pretty easily online. I'd start with credit quality and duration based on when you need the money back.

So bonds basically give you three solid perks: regular interest payments, way less drama than stocks, and they balance out your portfolio when everything else goes nuts. Honestly, I think of them as the dependable friend who's always there when you need them. Stocks tanking? Bonds usually do their own thing and keep you from losing your mind. They're perfect if you're gonna need that money soonish too. I'd probably put like 20-40% in bonds depending on how much risk makes you sweat at night.

So inflation expectations mess with bonds pretty badly - prices drop, yields spike. Investors get spooked about their money losing value, so they want better returns to make up for it. Long-term bonds get hit the worst since you're stuck with crappy rates for years. There's this thing called TIPS that actually protects against inflation by adjusting with it, which is pretty clever honestly. When building your portfolio, maybe shorten up those bond durations if inflation's looking sketchy. Or just throw in some inflation-protected stuff to hedge your bets.

So yield curves are basically your map for interest rates and bond pricing across different timeframes. They show how yields relate to maturity dates - longer bonds usually pay more because nobody wants their money tied up for decades at current rates, right? You can spot economic trends with them, price bonds against each other, and find trading opportunities. Honestly, inverted curves (when short rates beat long rates) often mean recession worries ahead. Watch for steepening or flattening - it'll help you position better. Pretty useful stuff once you get the hang of it.

Ugh, taxes are brutal on fixed income stuff. Corporate bonds and CDs get hit with ordinary income rates - way worse than capital gains. Municipal bonds dodge federal taxes though, which is pretty sweet even if the yields suck. Oh, and Treasuries skip state taxes at least. Here's the thing - I learned this the hard way - you gotta calculate what you're actually keeping after taxes. Makes a huge difference. If you can stuff bonds in your 401k or IRA, do it. The tax shelter is worth it.

So bond laddering is where you buy bonds that mature at different times instead of dumping everything into one maturity date. Like maybe 1, 3, 5, 7 years - spreads out your interest rate risk. When each one matures, you reinvest at whatever rates are available then. It's diversifying through time rather than just different assets, which honestly makes more sense than people realize. You can do equal amounts for each "rung" or focus on short/long-term only. First figure out your timeline and how much steady cash you actually need each year. Way better than trying to time the market.

So basically, when the economy's doing well, interest rates go up and that sucks for bond prices. But credit spreads get tighter, which is good. Flip side - in a recession, rates drop so bond prices rise, but then you've got way more credit risk especially with corporate stuff. Inflation's probably the worst part though since it just eats away at what your fixed payments are actually worth. I'd definitely spread things around - different credit qualities, different durations. That way you're not getting completely screwed if one scenario hits. Makes sense?

Yeah so corporate bonds are way riskier than government ones - companies can actually go belly up while governments just print more money or tax people harder. Plus when the economy tanks, corporations get hit first and default rates shoot up. Treasury bonds are basically the gold standard everyone compares everything else to. But here's the thing - you do get paid better yields for that extra risk, which is nice. I'd definitely spread it around though, like different companies and industries. Don't want to get burned if one sector implodes.

So municipal bonds are pretty sweet if you're looking at tax-free income. The interest doesn't get hit by federal taxes, and usually state taxes either if you buy local ones. Higher tax brackets make them way more appealing - like once you're at 24% or above, the math starts working in your favor big time. You'd calculate something called taxable equivalent yield to compare them fairly against regular bonds. Honestly, it's kind of cool that you're basically funding roads and schools while getting better after-tax returns than most taxable stuff.

So QE drives bond prices up and yields down - pretty straightforward supply and demand stuff. Central banks flood the market buying government and corporate debt, creating this huge artificial demand spike. Long-term bonds get hit hardest since that's what they're targeting. Corporate bonds do well too because investors can't find decent yields anywhere else, so they pile into riskier stuff. Honestly, it's been the same pattern since '08. The whole yield curve gets flattened out, which is why I'd focus more on credit risk than duration risk if you're repositioning. Duration becomes less of a factor when rates are getting suppressed artificially.

Start with duration and yield-to-maturity - they'll cover most of what you need for basic analysis. Credit spreads are super important for figuring out default risk. Modified duration helps when you're comparing bonds with different maturities. For callable bonds, you'll want to look at option-adjusted spread (OAS), though honestly that stuff gets pretty messy fast. Most people also track yield curve shape and do total return analysis for performance. Oh, and yield-to-worst is useful for return analysis too. I'd focus on duration and YTM first though - way less overwhelming to start there.

No Reviews